Coin Metrics' State of the Network: Issue 4

Intro and Updates

Dear crypto data enthusiasts,

Welcome back to this week’s edition of Coin Metrics’ State of the Network, an unbiased, focused view of the crypto market informed by our own network (on-chain) and market data.

This week, we would like to ask you to provide feedback on State of the Network and how we can improve. We’ve created a very brief and anonymous survey, and would appreciate your thoughts. You can complete the survey here.

Another busy week for Coin Metrics:

Released the updated version of the CM Reference Rates Methodology, adding nine new assets to the Coverage Universe. Here is our blog post about the release.

Earlier today, we announced a partnership with SMA to provide institutional grade crypto sentiment data. You can read the press release here.

A reminder that the Coin Metrics API v2.0 will be promoted to “stable” tomorrow (Tuesday, June 18th), resulting in breaking changes. Read the transition details here.

A reminder that Coin Metrics will be transitioning all of its legacy Community data infrastructure over to our Pro infrastructure tomorrow (Tuesday, June 18th). This will include the launch of a new API and the eventual shutdown of the existing Community API. Refer to the Community Upgrades section of this post for more information.

As always, if you have any feedback or requests, don’t hesitate to reach out at info@coinmetrics.io.

Weekly Feature

Tether’s Lead Grows as Facebook Looms

The stablecoin wars are upon us. There are now at least seven stablecoins with at least $25 million USD in daily transfer value, with new coins being announced at an increasingly rapid pace. None loom larger than Facebook’s new cryptocurrency, codenamed “Libra.” Poised to launch in 2020, Libra is likely to be used primarily for payments and is rumored to be a stablecoin (although it is yet to be confirmed).

But it will be entering a crowded market, that as of today is still dominated by Tether. We compared data across seven stablecoins (USDT, USDT-ETH, DAI, PAX, GUSD, TUSD, and USDC), to examine trends over the last 6 months and investigate stablecoin market share.

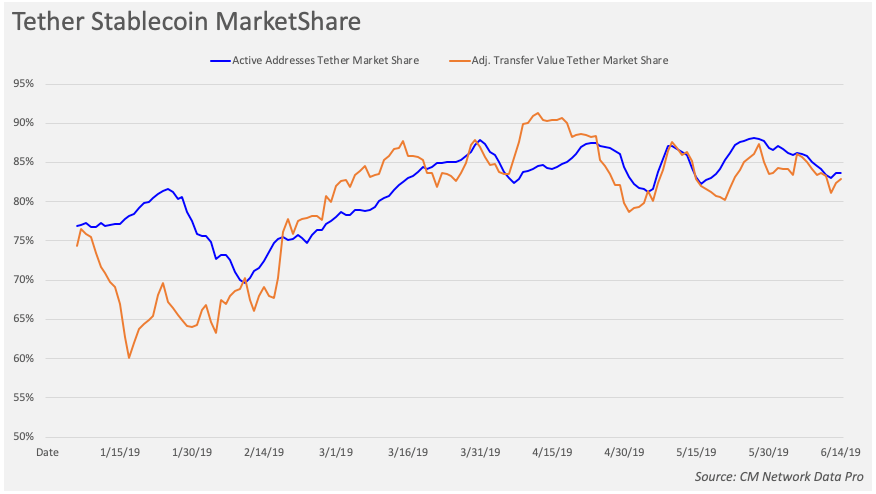

Tether’s Market Share

Tether’s dominance is trending upwards, with 83.69% of active addresses and 82.85% of adjusted transfer value as of June 14th.

As we noted in last week’s issue, Tether recently launched USDT on Ethereum (USDT-ETH), in addition to its original token (USDT) built on the Omni protocol. The below chart shows Tether’s market share (combining both USDT and USDT-ETH) compared to the combined market share of the remaining five stablecoins (DAI, PAX, GUSD, TUSD, and USDC) as measured by two metrics: active addresses (the number of unique addresses that were active in the network that day), and adjusted transfer value, which we define as the USD value of native units transferred that day, removing noise and certain artifacts like self-sends or deliberate spammy behavior.

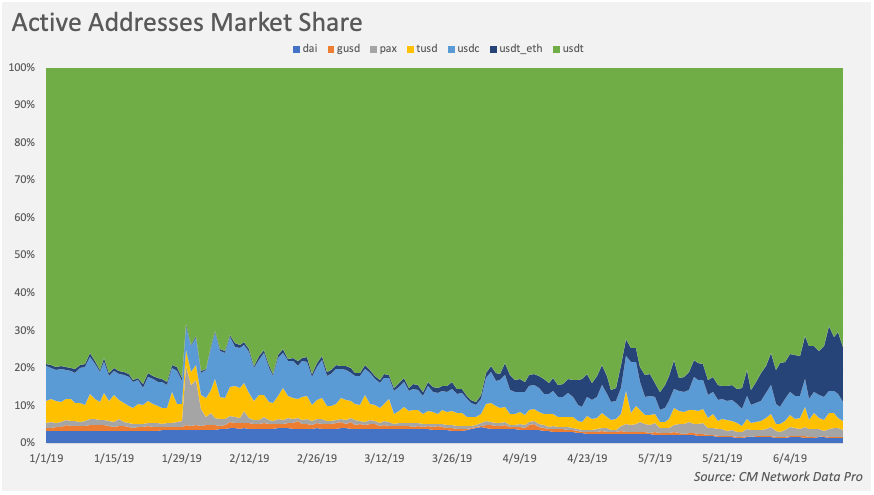

Active Addresses

Overall, the amount of total stablecoin active addresses is also growing. The below chart shows the total amount of daily active addresses across all seven stablecoins in our sample. Active addresses peaked at 66,898 on May 27th:

Interestingly, USDT-ETH just recently passed DAI and USDC in active addresses market share. While USDT still dominates, the Omni version of the token has actually been losing market share, as USDT-ETH has grown:

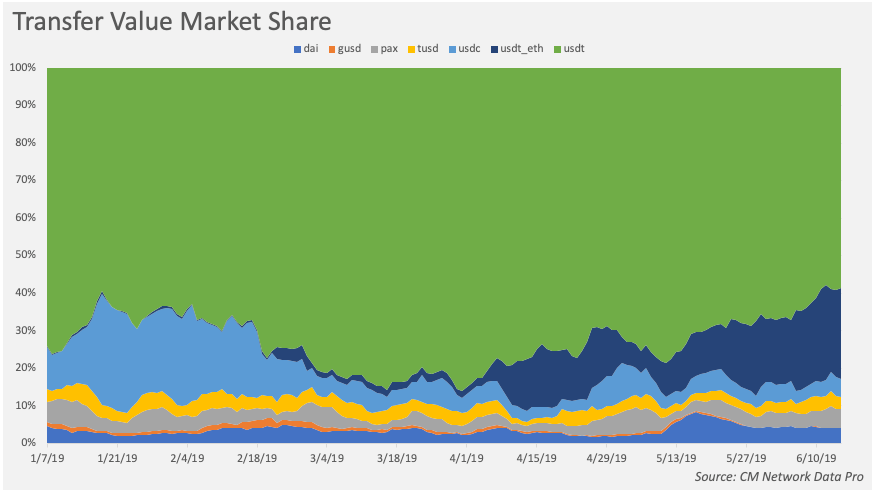

Adjusted Transfer Value

There have also recently been surges in stablecoin adjusted transfer value, reaching over $1.2 billion on May 24th. The below chart shows the combined (across all seven stablecoins) adjusted transfer value over the last six months:

Although Tether still leads in terms of adjusted transfer value, its lead is not quite as large. DAI currently has about 4% of the adjusted transfer value market share, while PAX and USDC each have about 5%.

While Tether still dominates the current stablecoin market, with new entrants such as Libra looming, it will be interesting to see how things look in a few months.

Network Data Insights

Summary Metrics

Mining Revenue

Network Highlights

On Friday June 14th, Bitcoin’s daily active addresses exceeded 1 million for the first time since Jan 19th, 2018. Meanwhile, its 1-year active supply appears to be growing again after 11 months of decline. Both signal potential positive momentum for Bitcoin moving into the second half of 2019:

Market Data Insights

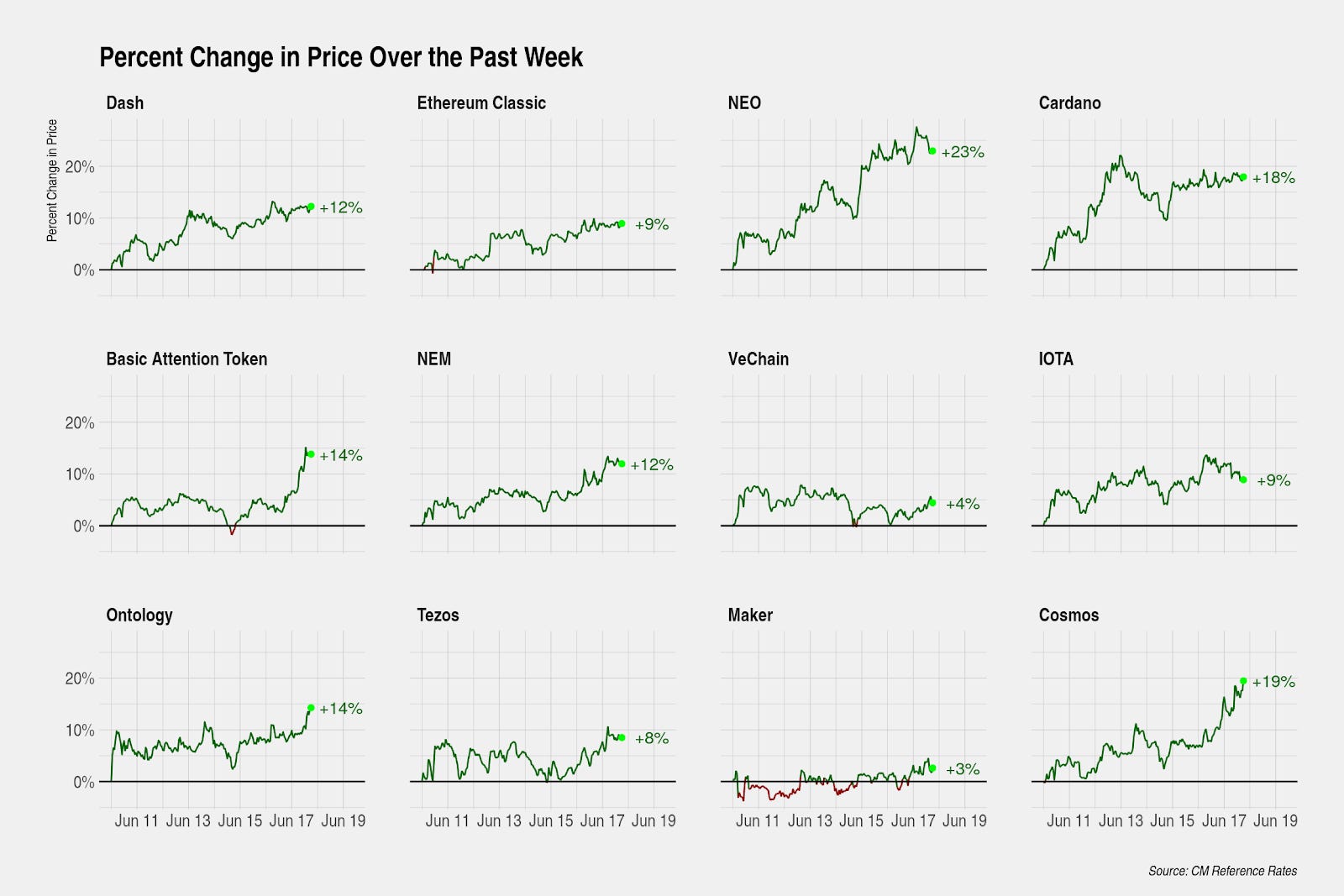

The market experienced another week of broad-based gains, with many assets up by 10 to 20%. Notable outperformers include ZCash (+33%), NEO (+23%), and Bitcoin (+22%).

The market reacted to the news on June 14 to a change in Binance’s terms and conditions in which they added a clause that “Binance is unable to provide services to any U.S. person”. The timing of this change closely coincided with an announcement by Bittrex on June 14 that it would further restrict an additional 42 assets from U.S. customers. Combined with a similar announcement earlier this month by Bittrex, this brings the total number of restricted assets to 74.

During this period, Bitcoin rallied on the news while many other assets at risk of being restricted for U.S. customers sold off, as market participants rightly interpret that the latest regulatory pressure will be beneficial for assets likely to remain available to U.S. customers. The market has since rallied to new weekly highs.

Bitcoin’s return of +22% is on the upper end of weekly returns of about 110 assets covered by the Coin Metrics Reference Rates, designed to be a transparent and independent source of pricing for portfolio accounting or research purposes.

At this point, the empirical data indicating that bitcoin and other crypto assets follow a bubble-and-crash cycle is quite strong. What is surprising in this market cycle is the speed and intensity of the returns given that many market participants believe that the current market cycle is in the beginning phases. For the month ending in May 2019, bitcoin realized a +62% return -- the third highest monthly return in five years. The only two monthly returns that exceeded this return occurred in the later half of 2017 when the bubble phase of the market cycle was well established. Seeing such strong returns this early in this market cycle represents a distinct shift from previous market cycles. By comparison, the recovery phase following the previous crash in late 2014 was characterized by steady and moderate gains.

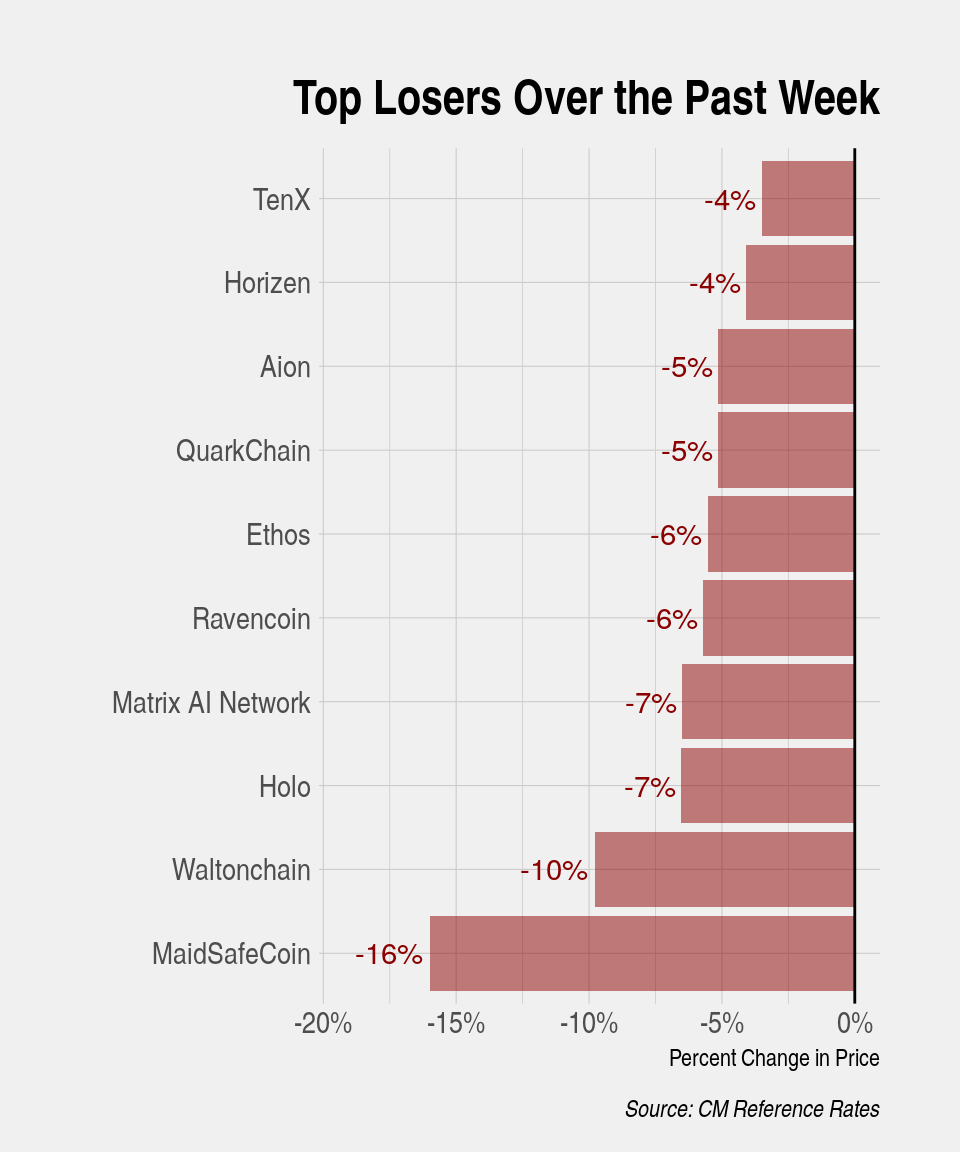

The exuberance of the recent market movement can also be seen by examining the top gainers and losers over the past week. The magnitude of the movements in Grin (+111%) and ChainLink (+90%) are reminiscent of the market environment last seen in late-2017. At this point, we are only seeing isolated incidents of market exuberance, however. Despite the broad-based rally, some assets are still declining in value suggesting that asset fundamentals are still playing a role in determining asset prices.

CM Bletchley Indexes (CMBI) Insights

Weekly Price Change

Insights

Below, we have mapped the Bletchley 10 Index values in both USD and BTC terms. You can see that while the index has more than doubled since the beginning of the year in USD terms, it has actually fallen relative to BTC, particularly in recent weeks because of BTC’s outperformance.

Subscribe and Past Issues

If you'd like to get State of the Network in your inbox, please subscribe here. You can see previous issues of State of the Network here.

Check out the Coin Metrics Blog for more in depth research and analysis.