Intro and Updates

Dear crypto data enthusiasts,

Welcome back to this week’s edition of Coin Metrics’ State of the Network, an unbiased, focused view of the crypto market informed by our own network (on-chain) and market data.

This week’s housekeeping items:

Coin Metrics’ legacy Community API will be shut down on July 15, 2019. If you are an existing legacy Community API user, you must switch to the new API before the 15th. You can find more details here: https://coinmetrics.io/announcing-our-community-data-upgrade/

Coin Metrics is hiring! Please check out our Careers page to view the openings

As always, if you have any feedback or requests, don’t hesitate to reach out at info@coinmetrics.io.

Weekly Feature

Introducing the RVTC Ratio

Metrics for evaluating crypto assets are still evolving. Initially, metrics from traditional equity markets, like float adjusted market cap, quickly became the norm. However the unique features of crypto assets allow analysts and observers to build new, more insightful, valuation metrics and ratios.

Last December, Coin Metrics introduced one such crypto-native valuation metric: the Realized Capitalization. A crypto asset’s realized cap is calculated by valuing each piece of the supply at the price at the last time it moved. In other words, it prices the supply at the time holders “realized” their gains or losses. Compared to market cap, the realized cap is smoother and changes much less abruptly:

Another crypto-native valuation metric is the “thermocap” (which is a reference to the total amount of energy expended by miners), which we define as the sum of all revenue (denominated in USD) that miners earned over the lifetime of the asset. It gives an estimate of the net fiat inflow into the asset.

The idea behind this is that miners should in theory operate slightly above breakeven. Miners’ costs are all denominated in their local fiat currency, but their revenue is only in crypto assets. Therefore, they must sell most of their newly mined assets and find fiat buyers for them. This idea mostly holds for Bitcoin and Ethereum. For smaller altcoins, miners probably first exchange for Bitcoin or a stable coin, and then for fiat.

Compared to Realized Cap, or market cap, thermocap is even more smoothed out as it can only grow as fast as the asset’s monetary policy allows. For most assets, this monetary policy entails ever decreasing issuance (in native units), which also affects the growth rate of the thermocap.

Rapidly after the introduction of Realized Cap, people began to study its ratio with the market cap. Adaptive Capital wrote that the fluctuations in the MVRV (market value vs realized value) could be used to determine whether a crypto asset is underpriced (if its market cap is much below the realized cap) or overpriced (if the realized cap is way above the market cap).

Studying the ratio of the realized value and thermocap (RVTC: realized value to thermocap) also turns out to yield valuable insights, and is much smoother than the MVRV. It’s particularly effective at picking out periods when an asset’s market becomes overheated.

Each peak in the RVTC locates the high of previous bubbles (one in 2011, two in 2013 and one in 2017). For Bitcoin, the ratio has a natural tendency to go up over time, as the ever decreasing issuance limits the growth of the thermocap.

The current value of this ratio confirms the consensus view among investors and participants in Bitcoin markets: the worst of the current bear market seems to be over.

Comparing the two ratios yields more insights. One thing to notice is that MVRV seems to build up before a spike, as the market price increases, the MVRV ratio goes up automatically while the RVTC ratio spikes very rapidly as on chain movements impact the realized cap.

Looking at the past months, the MVRV went from a bottom of 0.8 to 2.2 (+175%) while the RVTC went from 6.5 to 7 (+8%). This indicates that the recent price movement could continue, despite the realized cap being very close to its ATH.

This ratio can be extended to any asset that has mining, for example, Ethereum. Applying it to forks is still an open question as their thermocap only includes post-fork issuance whereas the realized cap still encapsulates some of the pre-fork history.

For Ethereum, the early months of the RVTC are omitted as they are very high. This is due to the fact that Ethereum started not from a blank state, but with already most of its supply issued. The realized cap was therefore very high compared to the thermocap.

We will continue to monitor the RVTC ratio moving forward, and expect it to keep yielding valuable insights over the upcoming months.

Network Data Insights

Summary Metrics

Crypto network activity declined over the first week of July, after a strong surge at the end of June. BTC, BCH, LTC, and XRP active addresses (which we define as the count of unique addresses that were active in the network either as a recipient or originator of a ledger change that day) all fell at least 13% week over week. ETH’s active addresses, however, remained steady at 333.6k, despite a 6% drop in total market cap.

On a positive note, hash rate continued to rise. Leading the way, BTC’s hash rate grow an additional 7%, even though BTC mining revenue declined by 4%. The decline in mining revenue is due to a 44% decline in transaction fees (mining revenue is composed of fees plus block rewards) as well as a decline in price.

Adjusted transfer value (which we define as the USD value of the sum of native units transferred that day removing noise and certain artifacts like self-sends or deliberate spammy behavior), however, dropped significantly. ETH’s adjusted transfer value is down 40%, which is the second biggest drop behind only LTC’s 61% decline.

Network Highlights

USDT-ETH’s active addresses reached an all-time high of 10,030 on July 4th, continuing its strong growth. USDT-ETH’s growth, however, has come at the expense of USDT (Omni), as we highlighted in State of the Network Issue 3:

Similarly, Paxos (PAX) activity has also been on the rise. PAX has seen a steady increase in daily active addresses since the beginning of May. This is likely due to PAX’s addition to Blockchain.com wallets, which was officially announced on May 1st:

Market Data Insights

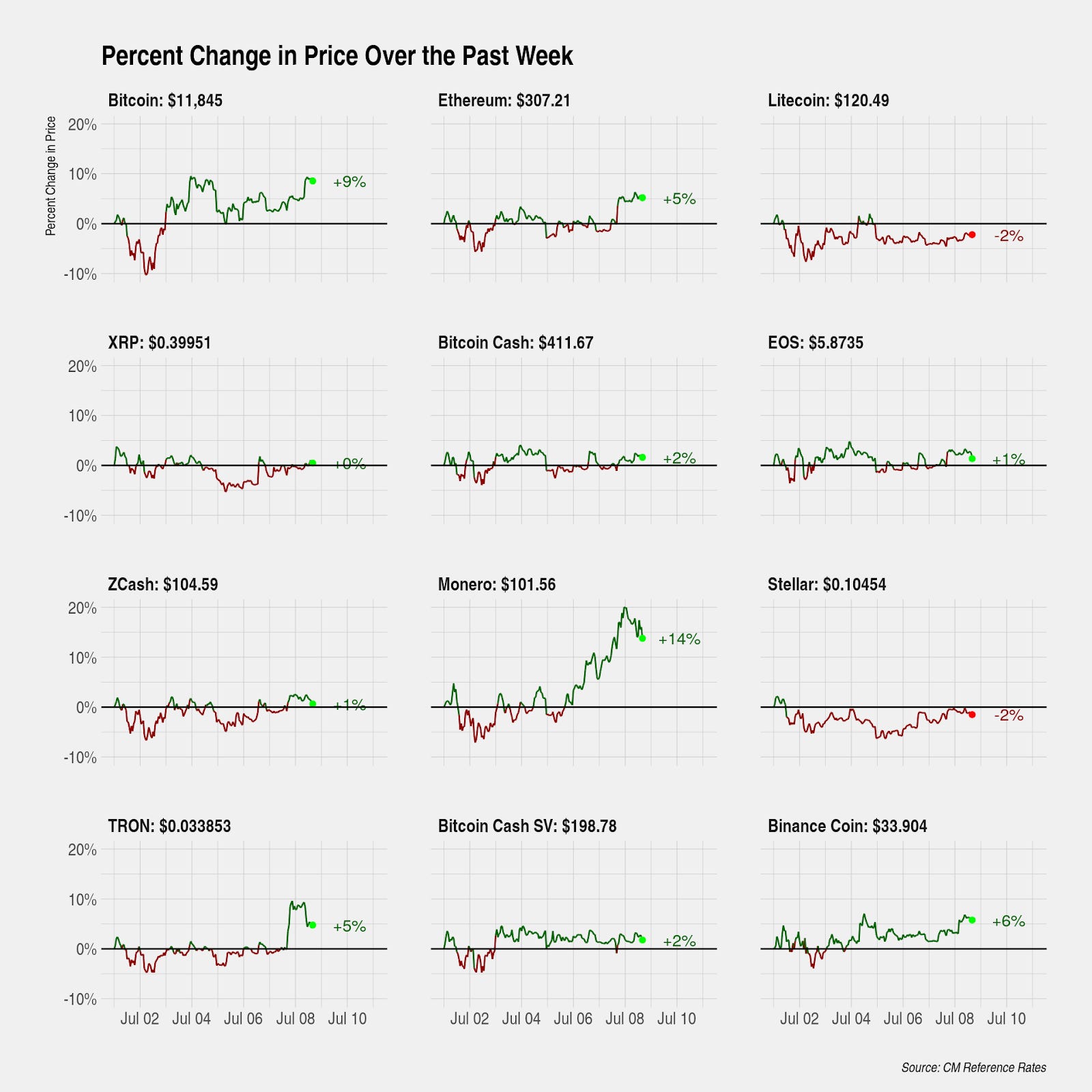

Larger capitalization assets continue outperformance of smaller capitalization assets over the past week with Bitcoin (+9%), Ethereum (+5%), Binance Coin (+6%) and Monero (+14%) leading the way. Smaller capitalization assets, however, have only experienced modest gains or even losses over the same period, indicating that the irrational exuberance of the past may have subsided.

Bitcoin, in particular, has been positioned to receive capital flows from two sources: as the primary on-ramp for fiat-based flows and as one of the primary quote currencies in markets for smaller assets. The slowing pace of new assets coming to market through initial exchange offerings has kept the growth in global supply muted. Capital and investor interest has remained mostly concentrated in Bitcoin:

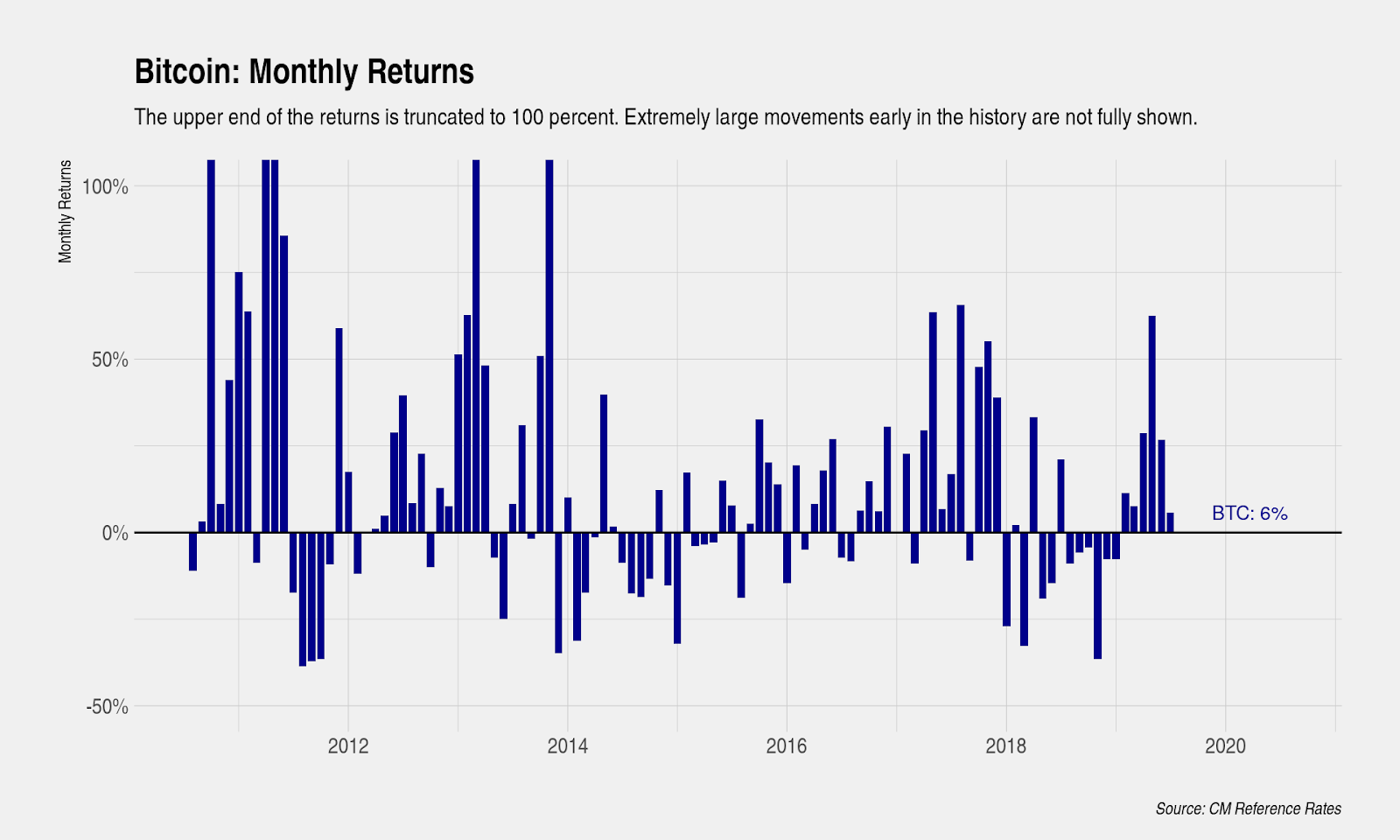

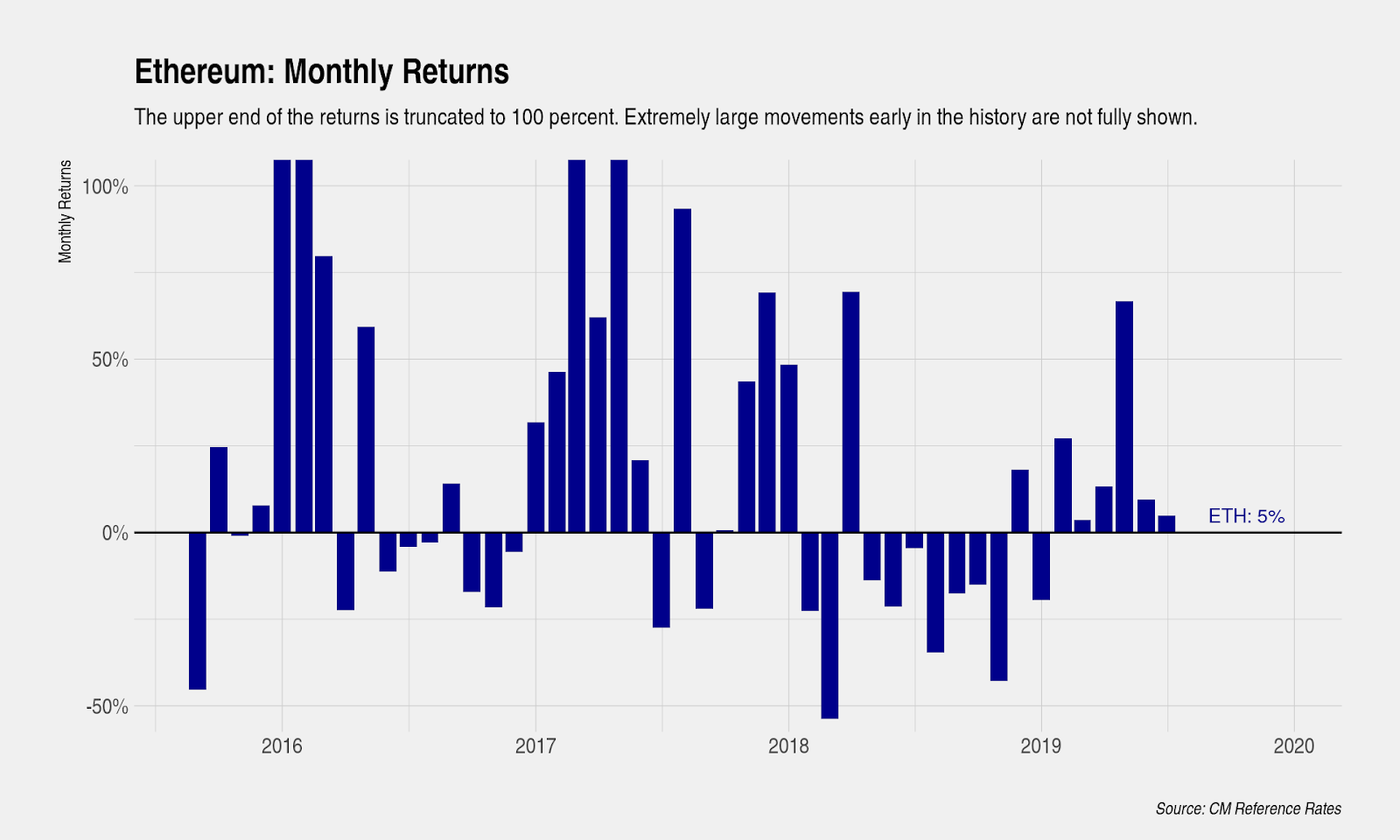

This cycle has been quite strong relative to previous cycles with both Bitcoin and Ethereum entering their sixth consecutive month of positive returns. If this month were to close with a positive return, this would tie the longest historical streak of positive monthly returns. Six consecutive months of positive returns has only happened three times in Bitcoin’s history and once in Ethereum’s, although shorter streaks of positive and negative returns are quite common in prices, highlighting the strong momentum effect in cryptocurrency markets.

CM Bletchley Indexes (CMBI) Insights

The CM Bletchley Indexes provide further evidence that the large cap crypto assets are still leading the market with the smaller less liquid assets struggling to keep up. This is demonstrated by the Bletchley 10 outperformed the Bletchley 20 which outperformed the Bletchley 40. Further, all indexes continued to lose value against Bitcoin and Ether, which both outperformed every index for the week:

Subscribe and Past Issues

If you'd like to get State of the Network in your inbox, please subscribe here. You can see previous issues of State of the Network here.

Check out the Coin Metrics Blog for more in depth research and analysis.