Coin Metrics' State of the Network: Issue 16

Tuesday, September 10, 2019

Weekly Feature

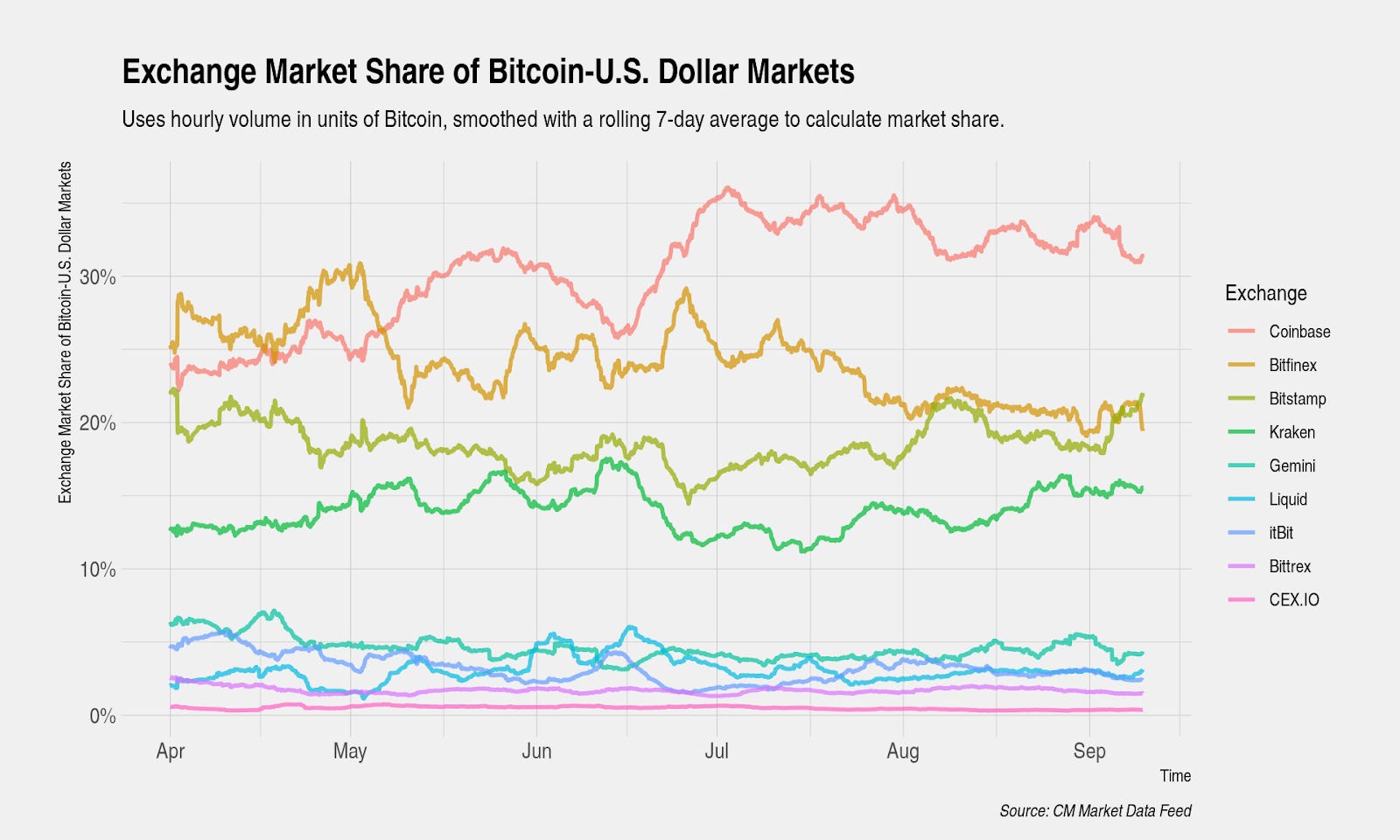

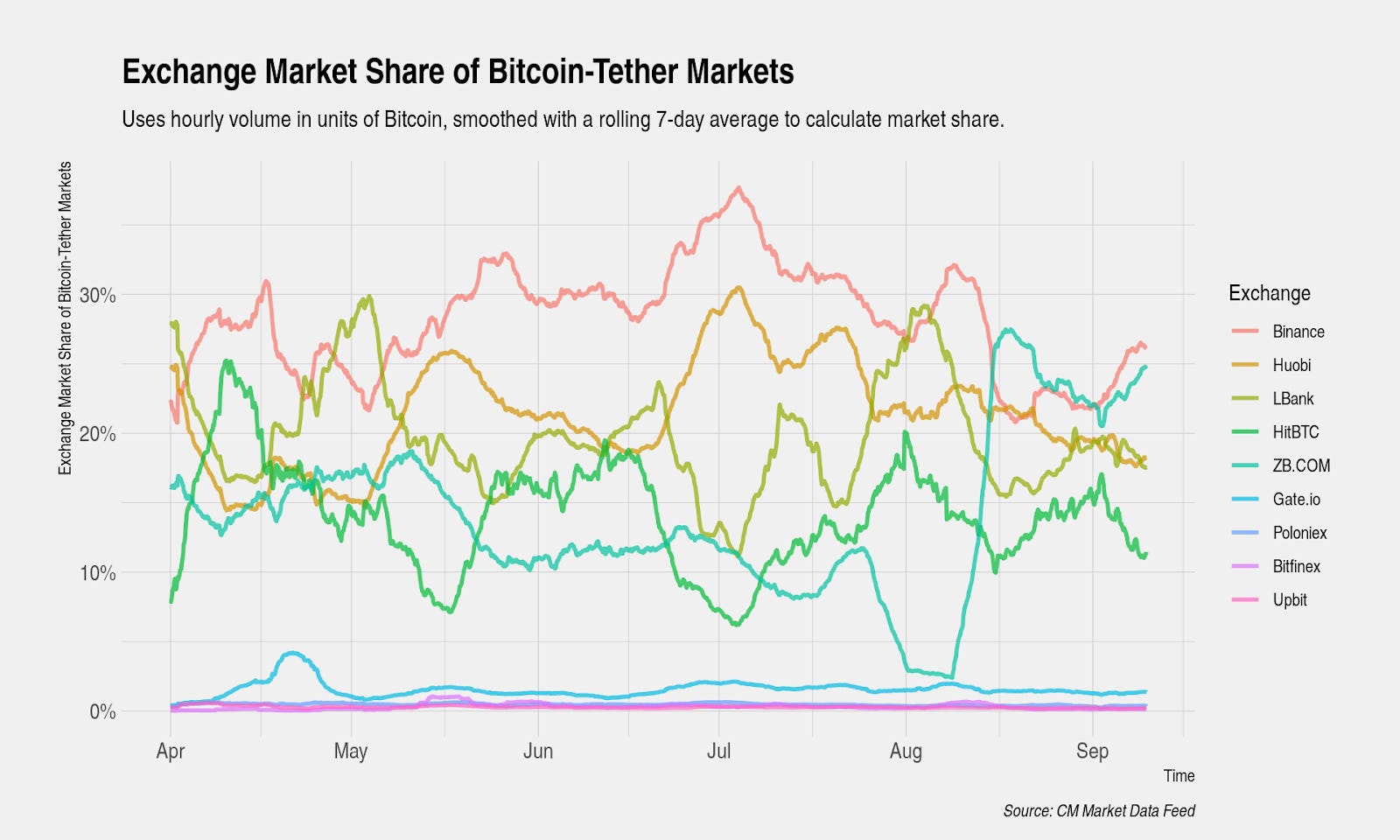

Bitcoin and Tether Volume Distribution by Exchange

Exchanges are a crucial piece of the crypto ecosystem. Successful exchanges can help fuel tremendous growth. But exchanges also represent potential systematic risks; if a popular exchange fails or is hacked, it affects the entire crypto market. This risk is amplified if trading is heavily concentrated in a single exchange, as was the case with Mt. Gox, which was reportedly handling 70% of BTC trading at the time it was hacked.

For this week’s State of the Network, we conducted an analysis of how Bitcoin and Tether trading volume is distributed among exchanges. Nine Bitcoin-U.S. Dollar (BTC-USD) markets and nine Bitcoin-Tether (BTC-USDT) markets were selected. Data from April 1, 2019 to present is used to examine the current state of cryptocurrency markets.

The following chart shows the volume of Bitcoin-U.S. Dollar markets by exchange where volume is defined as hourly units of Bitcoin, smoothed with a 7-day rolling average. The majority of trading takes place on Coinbase, Bitfinex, Bitstamp, and Kraken. In total, these four exchanges consist of roughly 85 percent of total traded Bitcoin-U.S. dollar volume. The remaining exchanges, including Gemini, itBit, and Bittrex each have volumes that are an order of magnitude less than Coinbase, the leading exchange.

Average hourly volume can vary greatly depending on price action and news-related catalysts. For example, Coinbase’s average hourly volume ranges from a low of 300 BTC to a high of 2,000 BTC during this time period.

Coinbase gradually increased its market share from 24 percent to 32 percent during this period, taking share primarily from Bitfinex which fell from 25 percent to 19 percent. Bitfinex’s reduction in market share is understandable given its longstanding issues with timely withdrawals and a heightened regulatory environment. As more exchanges limit access to U.S.-based traders, we expect more trading activity to concentrate on Coinbase, the primary Bitcoin-U.S. Dollar market.

Bitcoin-Tether markets show a similar level of concentration with trading activity heavily concentrated on Binance and Huobi. LBank, HitBTC, and ZB.COM also have moderate levels of reported volume, although Coin Metrics’ internal scoring framework indicates that these exchanges are likely to report a higher fraction of fake volume. In total, these five exchanges consist of roughly 95 percent of reported traded volume. Volume in Bitcoin-Tether markets are greater than Bitcoin-U.S. Dollar markets – Binance’s peak average volume is roughly twice the magnitude of Coinbase’s peak average volume.

Exchange market share for Bitcoin-Tether markets is volatile over short time periods likely due to inflated reported trading volumes by certain exchanges. Over this time period, the leading exchange has been held by three separate exchanges.

Network Data Insights

Summary Metrics

Bitcoin rallied this past week. It was up in every major metric except for adjusted velocity, which dropped by only 0.1%. Notably, BTC’s hash rate, mean difficulty, and total mining revenue continue to rise, which is a good sign for BTC’s overall network security. BTC realized market cap (realized capitalization is a metric created by Coin Metrics that is calculated by valuing each unit of supply at the price it last moved) also continues to grow, increasing by 0.7% week over week.

Realized cap decreased, however, for ETH, XRP, and LTC. ETH led the way with a 0.9% drop from last week, while LTC decreased by 0.5% and XRP dropped by 0.2%. XRP, LTC, and XRP continue to show high volatility from week to week, decreasing by 43.1%, increasing by 19.8%, and decreasing by 42.3% respectively.

Network Highlights

BSV’s realized cap recently surpassed $1 billion. As of September 8th, BSV’s realized cap is at an all-time high of $1,016,050,480.35.

However, BSV’s hash rate market share (compared to BTC and BCH) is approaching all-time lows. The following chart shows BSV’s percent share out of the total hash rate of BTC, BCH, and BSV combined.

Zcash’s (ZEC) hash rate recently hit an all-time high on August 13th. However, as ZEC’s hash rate has been growing, its active address count has been falling. The timing of this shift coincides with Bitmain’s introduction of an ASIC capable of mining ZEC in May, 2018, and ZEC’s vote against ASIC resistence in late June, 2018. This suggests that GPU miners were likely responsible for a lot of ZEC’s on-chain usage.

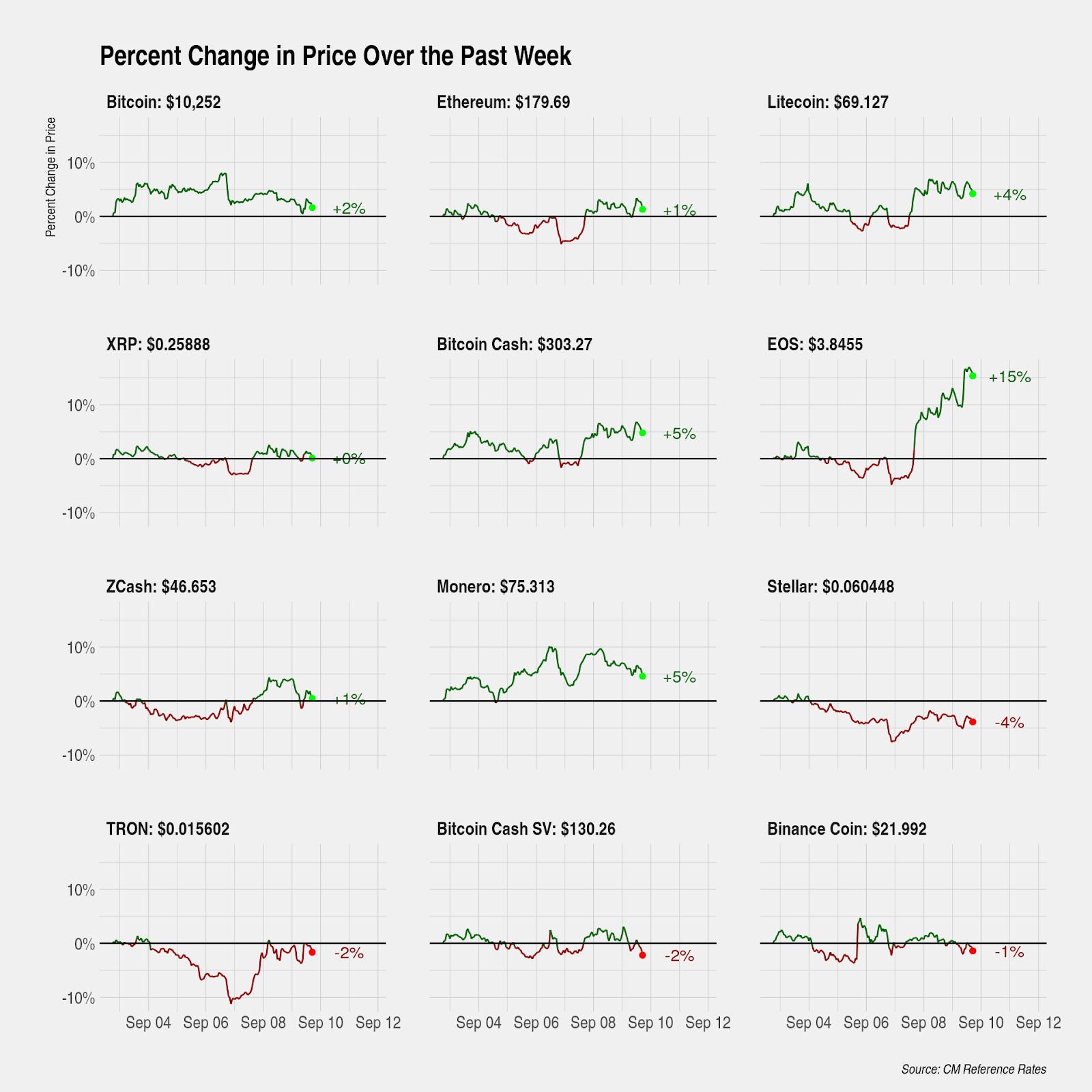

Market Data Insights

Some Signs of Assets Outperforming Bitcoin

Volatility was muted over the past week with the exception of few assets. Notable movers include EOS (+15%) and Cosmos (+31%). There was a brief moment over the weekend where some assets showed signs of outperforming Bitcoin, momentarily reversing the long-term trend of Bitcoin outperformance which started at the peak of the previous bubble.

Volatility Increasing Only for Bitcoin

Decreased trading activity for many assets has caused volatility to fall to all-time lows, or lows for this market cycle. Annualized volatility for many coins is now at a level similar to Bitcoin of around 80 to 90 percent whereas volatility during the previous peak regularly reached levels in excess of 200 percent.

Notably, only Bitcoin’s volatility has been increasing in recent months in part because of its inconsistent sensitivity to geopolitical and macroeconomic events, increased use of leverage via futures contracts, and the occasional attempts at engineered price movements.

Bitcoin Store-of-Value Thesis Revisited

Although in theory Bitcoin’s intrinsic properties make it a compelling store-of-value, empirical observations supporting this thesis are limited. While some of the limited empirical evidence is compelling, Bitcoin’s reaction function to macroeconomic surprises, geopolitical events, and safe haven flows is likely more complex than the standard narrative.

The latest observations show an inconsistent relationship between Bitcoin and gold. Gold has continued to rally this summer in response to flaring U.S.-China trade war tensions, anticipation of quantitative easing by the world’s major central banks, and central bank buying. But Bitcoin has stopped responding to the same events.

Earlier in the summer, the 30-day correlation between Bitcoin returns and gold returns peaked at +0.50, a level reached only two other times in its existence. Since then, correlation has dropped sharply to +0.15 which calls into question the stability of the Bitcoin store-of-value narrative.

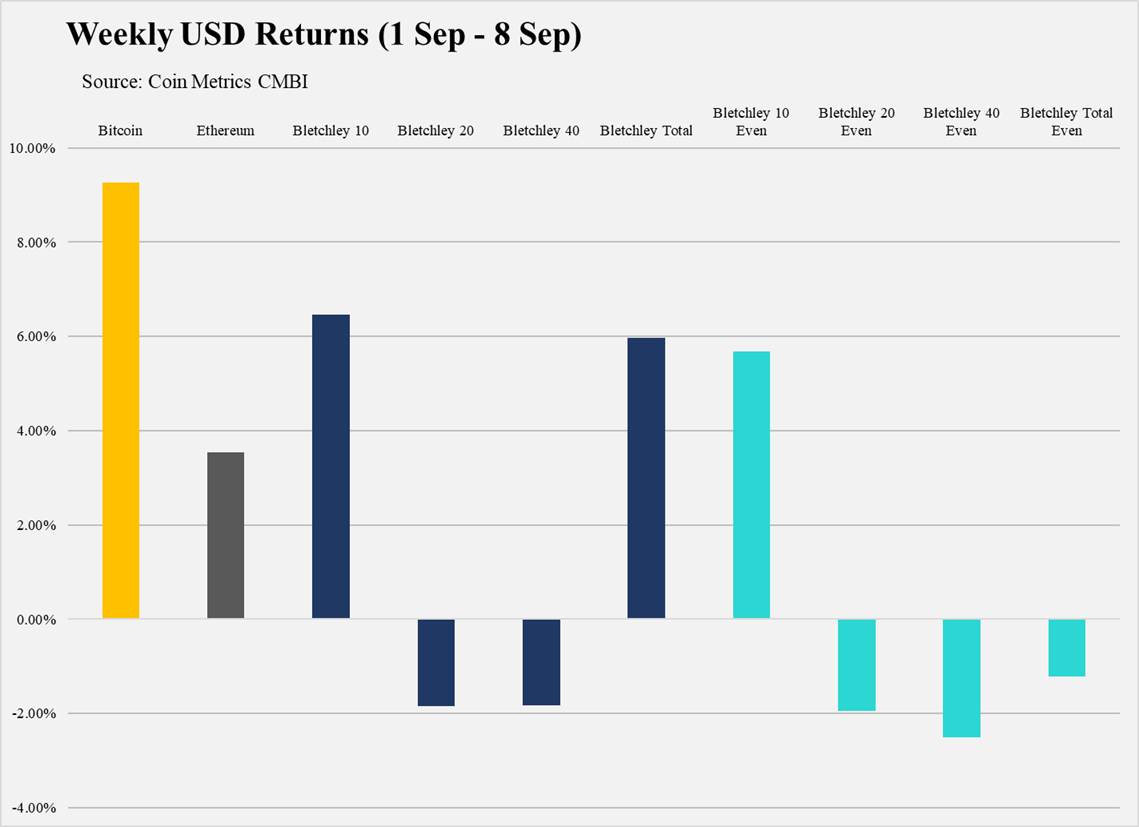

CM Bletchley Indexes (CMBI) Insights

This week the large cap crypto assets performed best, with the Bletchley 10 and Bletchley Total (which is 95% composed of the Bletchley 10) returning 6%. The mid cap and small cap markets stalled again with the Bletchley 20 and Bletchley 40 both returning -2% over the week. As has been the case for the majority of 2019, investors are finding the best returns chasing the liquidity of the large cap assets, with mid and small cap assets experiencing low buy volumes, leaving them susceptible to greater downside in market sell offs.

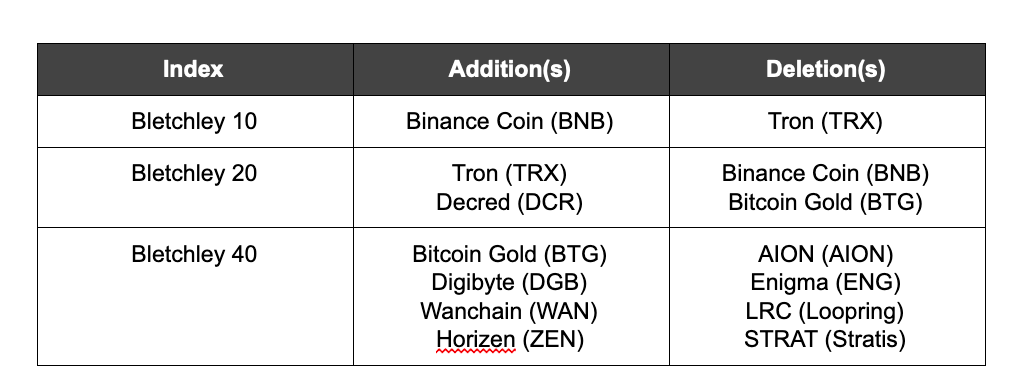

All Bletchley Indexes also experienced large turnovers in September, with the below changes being made. This level of turnover is a testament to the large levels of volatility that the asset class has experienced over the last month.

Coin Metrics Updates

This week’s updates from the Coin Metrics team:

Coin Metrics is hiring! We recently opened up 7 new roles, including Blockchain Data Engineer and Data Quality and Operations Lead. Please check out our Careers page to view the openings.

As always, if you have any feedback or requests, don’t hesitate to reach out at info@coinmetrics.io.

Subscribe and Past Issues

Coin Metrics’ State of the Network, is an unbiased, weekly view of the crypto market informed by our own network (on-chain) and market data.

If you'd like to get State of the Network in your inbox, please subscribe here. You can see previous issues of State of the Network here.

Check out the Coin Metrics Blog for more in depth research and analysis.