Coin Metrics' State of the Network: Issue 121 - The Rise of NFTs

Tuesday, September 21st, 2021

Get the best data-driven crypto insights and analysis every week:

The Rise of NFTs: A Data-Driven Overview of Non-Fungible Tokens

By Nate Maddrey and Kyle Waters

The following is adapted from an in-depth, data-driven research report covering the rise of NFTs. Access the full report here.

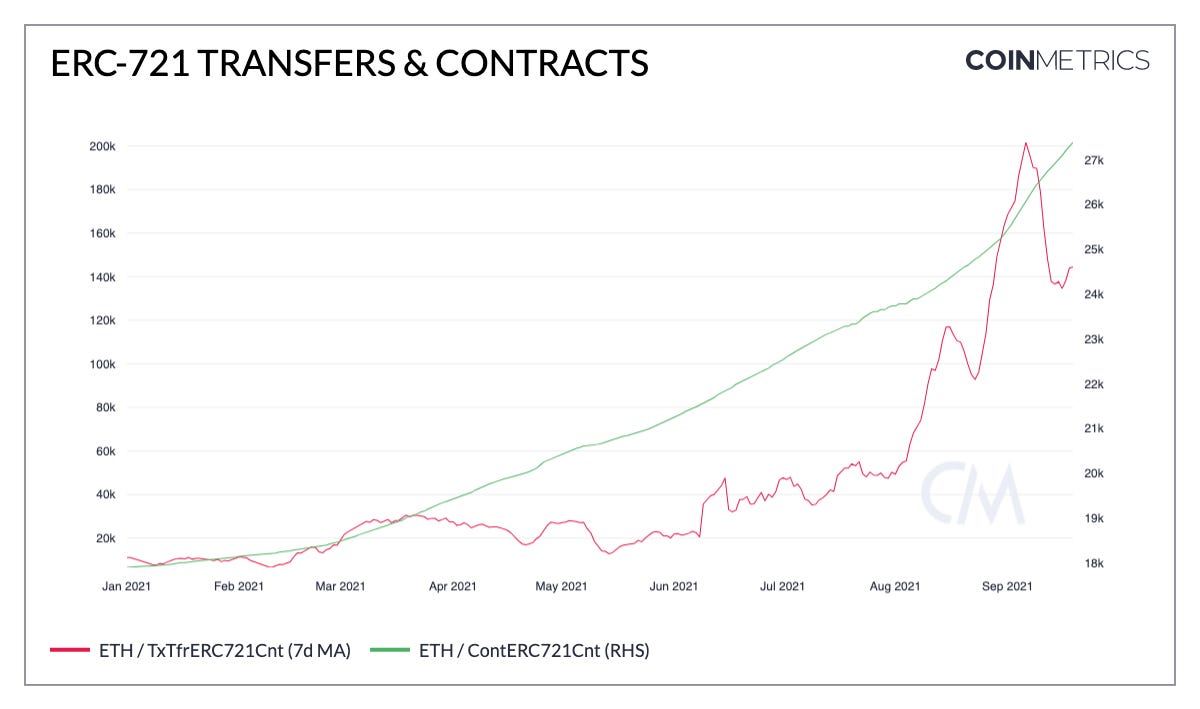

NFTs have become one of the most vibrant sectors of the burgeoning cryptoeconomy. With thousands of different NFT projects and more launching every day, NFTs now represent a material percentage of all activity on Ethereum. The daily number of ERC-721 transfers has increased by more than 10X from the beginning of 2021 to today, despite a recent pullback in activity.

Source: Coin Metrics Network Data Pro

To give a better sense of how this activity is broken down we selected a universe of NFT projects on Ethereum to study. The universe includes all relevant contract addresses for NFT marketplaces, projects in cryptoart, avatar picture projects (sometimes called PFPs or profile pictures), and other digital collectibles. Looking at the daily number of transactions by project it is apparent that most of the increased activity can be attributed to the rise of OpenSea as the top marketplace to buy, sell, and mint NFTs.

OpenSea has been the economic hub of NFT activity this year on Ethereum. The marketplace has grown at a staggering pace in 2021 attracting new users while facilitating the creation and exchange of NFTs. In August 2021, OpenSea registered over $3B in total volume, topping all historical sales volume combined in a single month. The number of unique buyers on OpenSea far eclipsed March 2021 highs in summer 2021, pointing to new widespread adoption.

While the number of unique buyers has fallen somewhat from an August 2021 high of ~35K unique addresses, there are still around ~20K unique addresses buying NFTs every day on OpenSea, about 6X more than the peak in March 2021. The number of daily sales on OpenSea also reached a high of ~80K in late August, more than 8X the high achieved in March.

While NFTs have attracted new users and generated new economic activity on Ethereum, they have also contributed to periods of network congestion and high fees.

Rising NFT activity has been highly correlated with increased median gas fees on Ethereum over the last few months. But simply observing these patterns does not confirm causal relationships. The impact of NFTs on gas fees is best understood at more granular levels after isolating idiosyncratic events. For example, on August 2nd, a new collection titled “Flowers” launched on the generative art platform Art Blocks Factory at 4pm UTC. The chart below shows that the mean gas price per block on August 2nd spiked immediately at 4pm as many clamored to mint the new NFTs.

There have been a few notable events this year indicating that institutional capital is starting to be deployed to NFTs and well-established firms are ready to explore the emerging space.

2021 has brought on the emergence of everything from NFT funds to an S&P 500 component purchasing an NFT for over $100K. Although NFT-focused funds have mostly been contained to existing crypto “native” investors, there has been some intriguing activity including Three Arrows Capital deploying thousands of ETH to buy up Art Blocks and launch of a $100M NFT fund called Starry Night Capital.

As NFTs’ share of economic activity in the crypto ecosystem grows, it is becoming increasingly important to track key metrics on the users and projects behind the proliferation of these digital goods. The charts below show the unique number of owners for each project over time.

Total unique owners is an important metric because NFT projects, like crypto networks in general, can benefit from network effects. A larger network of owners can command more cultural influence by having a broader set of supporters that are incentivized to promote the project or platform.

Notably, as CryptoPunks’ average price and volume has skyrocketed, the owner base has grown to around 3,000 unique owners today from only 1,000 at the beginning of the year.

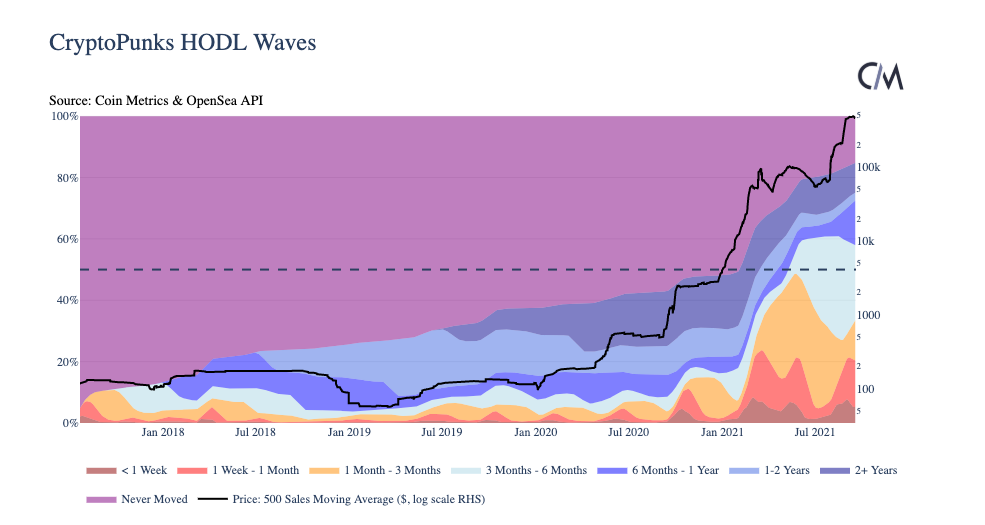

Additionally, measuring active supply for NFT projects can be used to give a sense if owners view the assets as long-term holds or short-term trades. One of the best ways to visualize active supply is by grouping coins into time bands indicating when they last moved (e.g. % of supply that moved in last week). These bands are often referred to as “HODL Waves”. For more on HODL waves, check out Coin Metrics’ primer covering On-Chain Indicators.

Below are the HODL waves for the CryptoPunks collection. Each colored band indicates the percentage of the CryptoPunks supply that moved (transferred, not necessarily sold) in that time period. The supply of CryptoPunks has been the most active it has ever been in 2021. At the end of May, about 50% of the 10K CryptoPunks had moved within the last 3 months (yellow+red+dark red bands) - corroborating the growth in unique Punk owners above. However, the 6-12 month band has been growing which could be a sign that buyers from earlier this year view CryptoPunks as assets to hold.

Although it has decreased in 2021, ~15% of the supply still has never moved from the wallets that first claimed the Punks. An even higher number of Punks have been transferred before but never sold. This has important implications for creating sound analytics, especially market capitalizations.

As the price tags for individual NFTs have become more eye-catching, there is a growing desire to measure the aggregate value of collections and compare market capitalizations for NFT projects. This is not a straightforward task however, even when compared to the challenges of finding market capitalizations of cryptocurrencies. The challenge for NFTs is in the name itself: each token is non-fungible or generally unique in some way with its own theoretical market price. On top of this, a singular item in a collection may sell infrequently or may have never been sold at all.

One way to estimate the market value of an NFT collection is by applying the “realized cap” methodology, first introduced and implemented to cryptocurrencies by Coin Metrics in 2018. A realized cap for NFTs would simply aggregate the last sale price for each NFT in the collection at each point in time it is calculated.

The table above illustrates how we calculate CryptoPunks' realized cap for a few given points in time. To find the realized cap on January 1, 2019, for example, we aggregate the last sale price (if any) for each CryptoPunk before that date. From the perspective of January 1st, 2019, Punk #1000 had most recently sold for $565 on December 26, 2017. Punk #4156 had last sold for $645 on September 17, 2018, Punk #4956 for $60, and so on for each of the 10K Punks in the collection. The last sale price for each punk is then added together to get the total realized cap at that point in time.

As of September 20, 2021, the realized cap of CryptoPunks is ~$780M.

Continue reading the full report…

Network Data Insights

Summary Metrics

Source: Coin Metrics Network Data Pro

BTC active addresses rose by 4% week-over-week while the number of ETH active addresses fell slightly. ETH fees have fallen after being at their highest levels since May in early September.

BTC and ETH hash rate continued to climb, with ETH hash rate at an all-time high. After 4 straight negative adjustments to BTC mining difficulty from May-July (which was the longest such streak since 2011), there have been 4 straight increases as hash rate recovers from the spring/summer crackdown on Chinese miners. BTC mining difficulty programmatically adjusts roughly every 2 weeks (2,016 blocks) to target a 10-minute average time between blocks.

Network Highlights

The market value to realized value (MVRV) ratio has historically been one of the most accurate on-chain indicators for gauging BTC market cycles. Throughout the 2013, 2017, and 2021 runs an MVRV of 3.0 or above has indicated a local price top. At the other end of the spectrum, an MVRV of 1.0 or below has signalled the best times to accumulate.

In addition to levels of 1 and 3, an MVRV of 2.0 is shaping up to be a potentially valuable indicator. Historically, an MVRV of 2.0 or above has aligned with the major bull runs. An MVRV below 2 has signalled bear territory. For example BTC MVRV crossed 2.0 on Dec 16th 2020 this year just as BTC price topped $20K for the first time. It dropped back below 2.0 on May 12th as news of China’s miner crackdown started to break.

BTC MVRV almost broke back above 2.0 on September 6th - it reached 1.94 as BTC spiked above $52K. But it has since dropped back down to about 1.73.

Source: Coin Metrics Formula Builder

ETH free float MVRV crossed above 2.0 on January 6th just after ETH climbed past $1,000. It dipped back below on February 22nd, then above again on April 28th as ETH pushed towards $4K. It fell below 2.0 on May 15th after the crash, and rebounded as high as 1.98 on September 5th.

Source: Coin Metrics Formula Builder

Coin Metrics Updates

This week’s updates from the Coin Metrics team:

Check out our market-data focused newsletter State of the Market, featuring weekly updates on market conditions.

The Coin Metrics mobile app provides real-time cryptoasset pricing and relevant on-chain data in a single app! Download for free here: https://coinmetrics.io/mobile-app/

As always, if you have any feedback or requests please let us know here.

Subscribe and Past Issues

Coin Metrics’ State of the Network, is an unbiased, weekly view of the crypto market informed by our own network (on-chain) and market data.

If you'd like to get State of the Network in your inbox, please subscribe here. You can see previous issues of State of the Network here.

Check out the Coin Metrics Blog for more in depth research and analysis.

© 2021 Coin Metrics Inc. All rights reserved. Redistribution is not permitted without consent. This newsletter does not constitute investment advice and is for informational purposes only and you should not make an investment decision on the basis of this information. The newsletter is provided “as is’ and Coin Metrics will not be liable for any loss or damage resulting from information obtained from the newsletter.