Coin Metrics' State of the Network: Issue 59

Tuesday, July 14th, 2020

Get the best data-driven crypto insights and analysis every week:

Weekly Feature

The following is an excerpt from an in-depth research report on the rise of stablecoins following the March 2020 crypto crash. Access the full report here.

The Rise of Stablecoins

By Nate Maddrey and the Coin Metrics Team

Stablecoin supply has exploded in 2020 but it’s unclear exactly why. After it took 5 years for stablecoin supply to reach 6 billion, it only took another 4 months for it to grow from 6 billion to 12 billion following the March 12th crypto crash.

A large majority of the supply growth was due to Tether. On March 12th 2020, the price of most crypoassets dropped over 50% after global equity markets crashed due to the rise of COVID-19. Within two weeks of the crash over 800M new USDT_ETH were issued. For context, about 740M USDT_ETH were issued from January 1st through March 11th. Additionally, USDT_TRX supply would increase by over 2B by the end of June.

Following the price crash, stablecoin markets were suddenly thrown into disarray. Stablecoin prices can fluctuate during times of market volatility due to sudden changes in supply and demand. For example, when Bitcoin price suddenly plummets, the demand for stablecoins often increases as investors look to move into a safe haven asset. This increased demand can cause the price of a stablecoin to rise above $1 on select exchanges.

The below chart shows stablecoin prices on an hourly basis (using Coin Metrics’ hourly reference rates) from March 11th through March 14th. The price of most stablecoins jumped up to between $1.03 and $1.06 from 2:00 to 6:00 UTC on March 13th. This corresponds with the timing of the BitMEX liquidation spiral, when Bitcoin price dropped to as low as $3,900.

USDT, USDC, PAX, BUSD, and HUSD appear to have recovered relatively quickly, returning close to their $1 pegs within days after the crash. But as seen in the below chart, USDT’s price remained above $1. Notably, USDT’s price remained significantly higher than USDC, PAX, BUSD, and HUSD through mid-May (DAI and GUSD are excluded from the following chart due to their extreme divergence).

Because of their nature as price-pegged assets, deviations in stablecoin prices create arbitrage opportunities. For example, when a stablecoin’s price is above $1, new supply can be printed at $1 each, and then sold on an exchange for a profit. Done at a large enough scale, this can lead to significant profit even if the price is only slightly over a dollar.

Continue reading the full report...

Network Data Insights

Summary Metrics

Bitcoin (BTC) and Ethereum (ETH) continued to show positive momentum this week, with small growth in usage metrics including active addresses and transactions.

But the smaller-cap assets noticeably outperformed this past week. Ripple (XRP), Litecoin (LTC), and Bitcoin Cash (BCH) all grew more week-over-week than BTC and ETH in most usage, valuation, and economics metrics. XRP led the way in many categories, including a 14.8% growth in active addresses and 11.8% growth in market cap.

Is this a sign of an altseason? We explore in this week’s Network Highlights and Market Data Insights sections.

Network Highlights

In addition to Ripple, Litecoin, and Bitcoin Cash, many other mid to small cap cryptoassets saw increased activity over the last week. Often described as a “meme coin,” Dogecoin (DOGE) had a large increase in market capitalization on July 7th and 8th. This corresponds with a viral TikTok video that promoted DOGE.

DOGE two-year revived supply also spiked on July 8th. Over 1B units of supply that had not moved on-chain for at least two years were suddenly transferred. This suggests that some longer term holders sold off amidst the frenzy.

DOGE active addresses have been surging in July but are still below 2020 highs. Network usage is not increasing as fast as valuation, a potential signal of a price bubble.

Cardano (ADA) has also been growing recently. In anticipation of the Shelley mainnet release, ADA’s market cap reached new 2020 highs on July 8th. Cardano’s market cap has passed LTC’s, despite having about 7x less daily active addresses.

Market Data Insights

This week marked a roughly $13.9B, or nearly 38%, uplift in spot volume. This is a remarkable number when considering the historically low volatility range that BTC and ETH have been trading in. Low volatility generally coincides with low volume but in the past week, the speculation on a few key altcoins pushed trading volumes upward. In this analysis, we will focus on three in particular: Doge, Cardano and ChainLink. Together they made up 20% of this week’s increase.

Let’s take a look at some exchanges that benefited the most, beginning with the more well known exchanges that support a long tail of altcoins. Binance, Bittrex, Kraken and Poloniex all benefited from these assets. Binance, Bittrex and Kraken saw a fairly equal distribution between all three assets, similar to the overall uplift contributed by these assets to the total spot volume for all exchanges.

Poloniex saw 57% of its weekly increase in volume from Doge trading. The exchange has one of the longest standing Doge markets and was the primary trading venue for the Doge spike in the summer of 2019. Regardless of a historically liberal listing policy, Poloniex does not currently support Cardano and missed a large opportunity this past week. Given that they have prioritized the listing of lesser known assets recently such as BitCherry and Flexacoin, it brings into question the exchange’s listing strategy.

Coinbase also saw a large portion (39.5%) of this week’s gain in volume attributed to ChainLink. Often considered to have a fairly liberal listing strategy and primarily U.S. retail trading base, this large portion of trading attributed to ChainLink may signal that we are still in the midst of an altseason and that even small traders are embracing a risk-on investing strategy.

CM Bletchley Indexes (CMBI) Insights

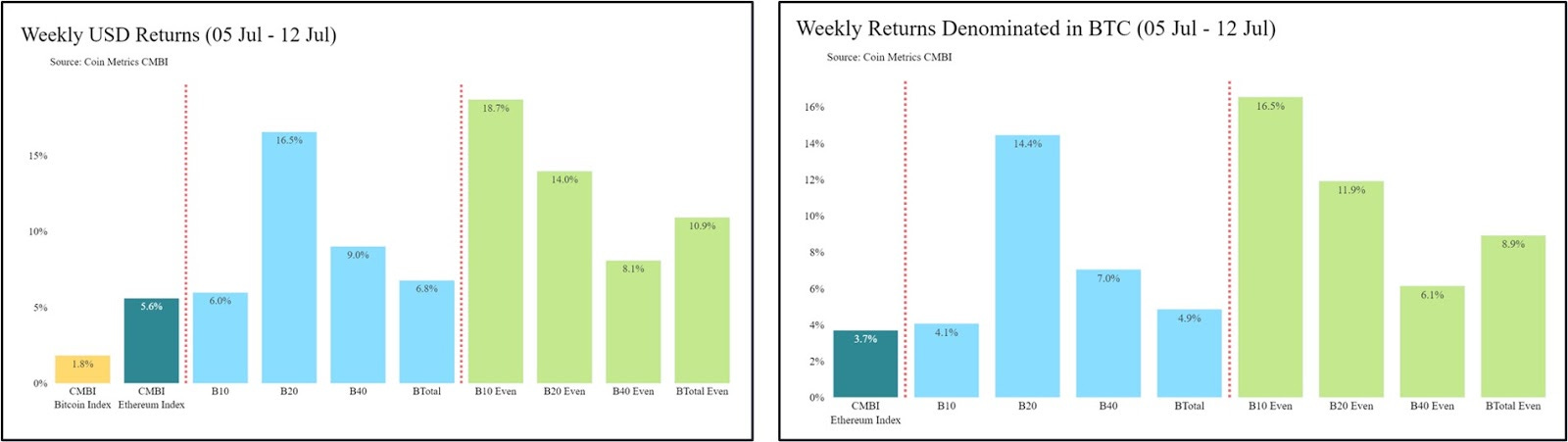

For the first time in 5 weeks, all of the CMBI and Bletchley Indexes experienced positive returns week on week. The CMBI Bitcoin Index Continued to demonstrate a low level of volatility, returning 1.8% for the week, marking the 6ths consecutive week of less than |±3%| performance. The CMBI Ethereum Index had a better week, returning 5.6%. But it was the multi-asset indexes that had the best performances, returning between 6.0% (Bletchley 10, Large Cap) and 16.5% (Bletchley 20, Mid Cap) during the week.

Despite the low volatility of Bitcoin, it was the Bletchley 10 Even Index that was the best performer, returning 18.7%, largely due to the strong performances of Chainlink and Tezos. In an even weighted index, all constituents are weighted evenly at the time of rebalance, thus applying a higher weighting to the lower market cap assets than a market cap weighted index (which for the Bletchley 10 weights Bitcoin 71%).

For further detail on the performance of the CMBI Bitcoin Index and CMBI Ethereum Index, please check out the CMBI Single Asset Index Factsheet.

Coin Metrics Updates

This week’s updates from the Coin Metrics team:

Coin Metrics is hiring! Please check out our Careers page to view the openings.

As always, if you have any feedback or requests, don’t hesitate to reach out at info@coinmetrics.io.

Subscribe and Past Issues

Coin Metrics’ State of the Network, is an unbiased, weekly view of the crypto market informed by our own network (on-chain) and market data.

If you'd like to get State of the Network in your inbox, please subscribe here. You can see previous issues of State of the Network here.

Check out the Coin Metrics Blog for more in depth research and analysis.