Coin Metrics’ State of the Network: Issue 178

Tuesday, October 25th, 2022

Get the best data-drive crypto insights and analysis every week:

Understanding Crypto Asset Scarcity Through the Data of Forked Blockchains

By Matías Andrade, Kyle Waters, and Nate Maddrey

Among all the innovations brought about by cryptography, it is the creation of indisputable scarcity that allowed for the creation of cryptocurrencies. Satoshi’s great innovation was the idea that through a cryptographic protocol and a rigorous economic incentive mechanism a distributed ledger could be agreed-upon to create assets that could only be used and spent by a single user. In the age of digital technologies, copy-paste, and open-source code, the great innovation encoded in Bitcoin and in later crypto assets was a concept that was alien and absurd in the digital world: scarcity. And yet, opponents of crypto assets in general argue that Bitcoin—and all other crypto assets—are not inherently scarce, since the code can be copied to create an instantiation of an asset that is functionally equivalent to Bitcoin. In today’s State of the Network, we set out to examine this view and understand how similar instances of an asset code-base are used and adopted completely differently, using forked chains as a natural experiment of sorts. Do these forked chains receive as much use as the original instantiation? What is their rate of adoption? In particular, we will look at Litecoin, Ethereum Classic, and Bitcoin Cash as (in)famous examples of forked chains to illustrate the true nature of digital scarcity.

Bitcoin / Litecoin

Litecoin is one of the oldest crypto assets out there, created in October of 2011 by ex-Google employee Charlie Lee. It was a direct Bitcoin fork, taking all the design principles of Bitcoin while slightly modifying it to be more quick processing blocks for use in small transactions. It has an average block time of around 2.5 minutes (¼ that of Bitcoin) with a total supply cap of 84 million LTC, 4x that of Bitcoin. In addition to these characteristics, Litecoin is based on the scrypt hashing algorithm, compared to Bitcoin’s SHA256, which is incompatible with Bitcoin’s ASICs and was initially most efficiently mined using GPU cards. Litecoin featured a “fair launch,” with little to no pre-mined LTC. Litecoin was a non-contentious fork, and its genesis was not the product of infighting within Bitcoin, nor did it set out to outperform or replace Bitcoin, but simply fill in a niche that would be complementary to Bitcoin.

Although Litecoin has been described as silver to Bitcoin’s gold, its value has ranged widely with little to no relationship to Bitcoin’s value, a sign that this metallic analogy is somewhat inaccurate in view of the broad market data we have today. Although their prices have tended to move together closely directionally, LTC’s total value has not kept pace with BTC. Below, we present the realized capitalizations of the two assets:

Source: Coin Metrics Formula Builder

However, Bitcoin’s relationship with Litecoin is closer than this market view would suggest. Litecoin has been used as a testnet of sorts for Bitcoin upgrades, since they mostly share a common codebase, and both SegWit and the Lightning Network were successfully tested on the Litecoin network before being implemented on the Bitcoin network. In 2022, Mimblewimble was introduced to Litecoin; if successful, it could similarly be adopted by the Bitcoin codebase sometime in the future.

Ethereum / Ethereum Classic

One of the most infamous of splits, Ethereum Classic was born from the chaos of the hacking of “The DAO”, an early darling Ethereum project turned disaster. Originally envisioned as a decentralized venture capital fund, The DAO attracted millions of ETH in deposits in 2016. But unbeknownst to contributors, the codebase of The DAO contained a fatal vulnerability that allowed an attacker to suddenly steal nearly all user funds through a reentrancy attack. Like a faulty ATM, the exploiter was able to siphon millions of ETH from The DAO (the full events of The DAO hack are well documented and recounted in books like Laura Shin’s Cryptopians and Camila Russo’s The Infinite Machine).

The severity of the hack led to an emergency fork of Ethereum in July 2016 “resetting” The DAO hacker’s address and allowing for recovery of the stolen funds. This was a highly contentious fork with a small but staunch contingency forming behind a belief that “Code is Law”, rejecting what they believed was a decision that could undermine Ethereum’s basic assurances. With this support group, some miners started working off the “original” chain that was not touched and allowed the hacker to keep the funds, which came to be known as Ethereum Classic (ETC).

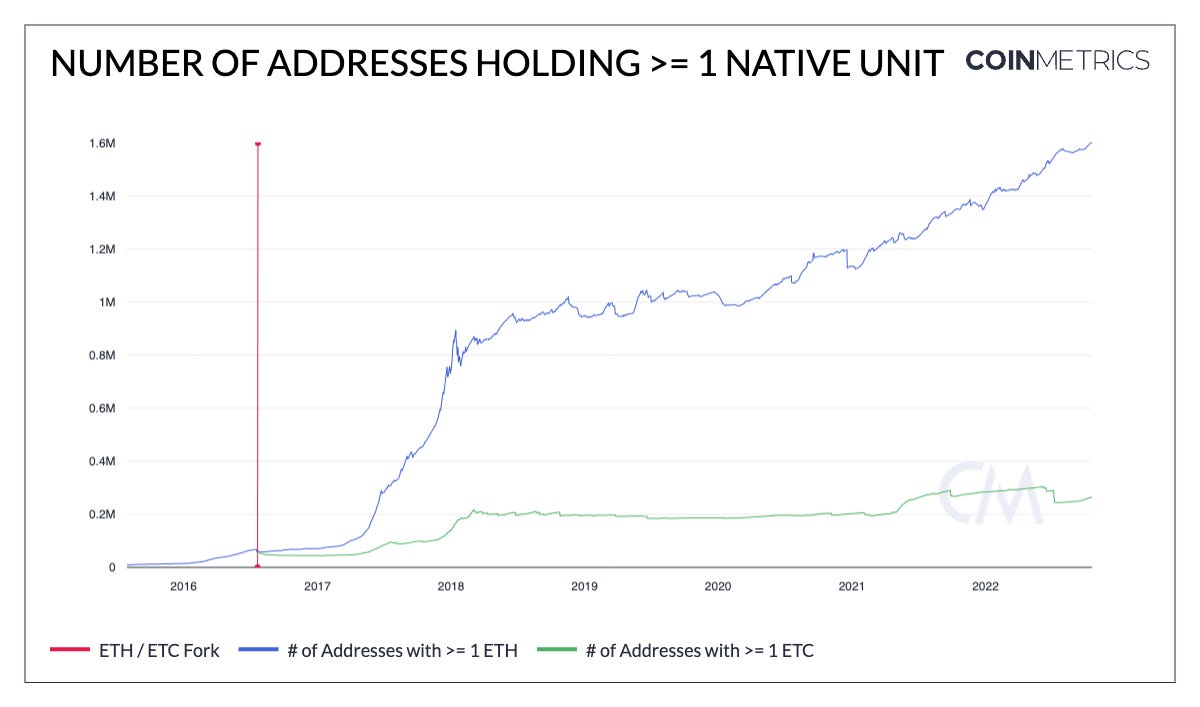

But in the years since The DAO fork, it is very clear from the data that Ethereum Classic has failed to attract even a fraction of the same level of developer and user adoption as Ethereum. The chart below shows the number of addresses holding at least 1 ETH or ETC. ETH adoption has continued to push upwards while ETC address growth has stagnated. The number of addresses holding at least 1 ETH today is about 1.6M while the number of addresses holding at least 1 ETC is 267K.

Source: Coin Metrics Formula Builder

Meanwhile, Ethereum settles amounts on-chain that are orders of magnitude higher than Ethereum Classic. Taking into account stablecoins and other major tokens, Ethereum is a far more economically meaningful ecosystem.

Source: Coin Metrics Formula Builder

It’s unclear what ETC is actually used for today. While Ethereum’s Dapp ecosystem has flourished, there are no stablecoins on ETC, popular DeFi protocols, or NFT marketplaces, despite its similarity to Ethereum.

Bitcoin / Bitcoin Cash

Another contentious fork, Bitcoin Cash is one of the most infamous coins to come out of Bitcoin’s codebase since it emerged as a result of vicious technological and ideological debates during the 2017 “Blocksize Wars.” This debate was catalyzed by the BIP-141 “Segregated Witness” proposal to introduce a new transaction type into Bitcoin with the end goal of achieving greater scalability and transaction throughput with Layer-2 solutions such as the Lightning Network. This upgrade set off a debate between parties that believed that Bitcoin should achieve scalability through larger block sizes at the cost of decentralization—since larger block sizes favor better-capitalized and more sophisticated miners. They based this preference for scaling of the base-layer, among many other reasons, on Satoshi’s vision of Bitcoin as a form of cash, i.e. an asset that you could use to transact on a daily basis (for example, to purchase a cup of coffee). It was this group of users and miners that eventually led to the creation of Bitcoin Cash.

Source: Coin Metrics Formula Builder

The introduction of SegWit created the potential for a contentious fork, since miners could abstain from upgrading the software to the new version, as well as implement software changes of their own. A large commercial group of miners and users tried to block the upgrade from being integrated into the Bitcoin mainchain, even though SegWit (BIP-141) constitutes a soft-fork and thus retained backwards-compatibility with existing clients and miners. Although the upgrade eventually went through and Bitcoin is able to fit more transactions-per-block—as well compatibility with the Lightning Network—Bitcoin Cash emerged as a fork with 8MB blocks and a more dynamic difficulty-adjustment mechanism. Although the 8MB blocks give Bitcoin Cash a greater transaction throughput compared to Bitcoin (excluding Lightning Layer), it is clear from the chart above that this additional capacity is nowhere close to being fully utilized. Although bitcoin ranges between 70-80% utilization as of today, Bitcoin Cash hovers below 10% utilization. In addition, even if BCH blocks fit more transactions, the weaker settlement assurances of the chain require users to wait longer for transaction confirmation and settlement.

Conclusion

The examples presented above show that nuance is required before critiquing the scarcity of cryptocurrencies. While it is true that anyone is free to create their own copy of an open-source project like Bitcoin or other protocols, it is not guaranteed that users will choose to deem it valuable or worth adopting. In practice, the validity and success of a blockchain fork is grounded in social consensus; their efficacy limited by the strength of user network effects, chain security, and a common Schelling (focal) point in absence of centralized communications.

Network Data Insights

Summary Metrics

Source: Coin Metrics Network Data Pro

Bitcoin active addresses averaged 873K per day over the last week, a 2% decline from the previous week. On Ethereum, active addresses fell a bit sharper with a 14% decline week-over-week to 480K/day. The average gas price on Ethereum has creeped up though lately, with the the 7d daily average hitting 27 GWEI, the highest since July.

Coin Metrics Updates

This week’s updates from the Coin Metrics team:

For the best in-depth discussion of CM data and research, come check out our research community on the web3 social media platform gm.xyz.

As always, if you have any feedback or requests please let us know here.

Subscribe and Past Issues

Coin Metrics’ State of the Network, is an unbiased, weekly view of the crypto market informed by our own network (on-chain) and market data.

If you'd like to get State of the Network in your inbox, please subscribe here. You can see previous issues of State of the Network here.

Check out the Coin Metrics Blog for more in depth research and analysis.

© 2022 Coin Metrics Inc. All rights reserved. Redistribution is not permitted without consent. This newsletter does not constitute investment advice and is for informational purposes only and you should not make an investment decision on the basis of this information. The newsletter is provided “as is” and Coin Metrics will not be liable for any loss or damage resulting from information obtained from the newsletter.