Coin Metrics’ State of the Network: Issue 199

Tuesday, March 21st, 2023

Get the best data-driven crypto insights and analysis every week:

An Introduction to Liquid Staking

By: Tanay Ved & Matías Andrade

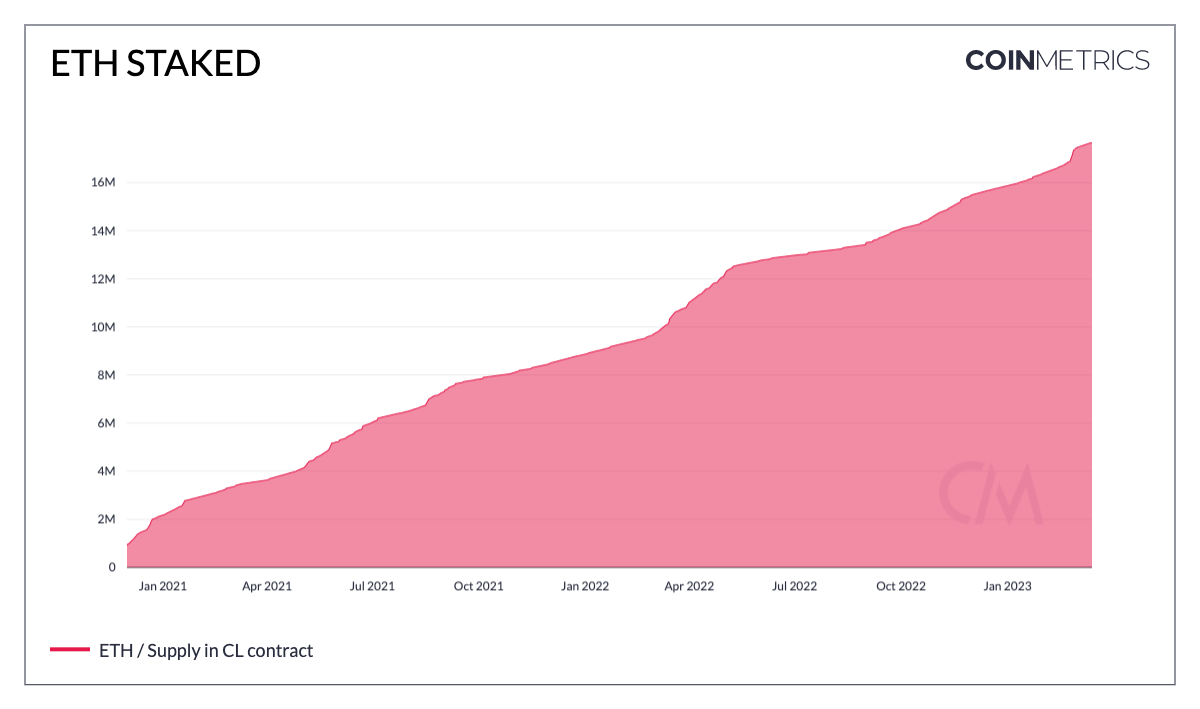

Ethereum’s transition to a Proof-of-Stake (PoS) based blockchain through The Merge has been a pivotal landmark in its existence, bringing about fundamental changes to the network's security and economics. With the role of primary economic actors in a PoS system falling on validators (i.e., stakers), these actors are incentivized to ‘stake’ or lock up their ETH to secure the network and earn staking rewards in the form of block rewards and transaction fees. Since The Merge on September 15th, 2022, the amount of ETH staked has risen to ~17.5M.

With Ethereum’s next major upgrade in the form of the Shanghai hard fork fast approaching, staked ETH and accumulated staking rewards that have been locked thus far, will be available to “unstake” or redeemable via a systematic exit period. The problem of managing illiquid staked assets before the upgrade has paved the way for an ecosystem of liquid representations of staked ETH—bringing the rise of a set of digital assets known as Liquid Staking Derivatives. In this issue of State of the Network, we introduce the need for this growing solution, highlight major players in the market with their varying approaches, examine potential risks, and finally peek into exciting primitives emerging to meet the demand for staking.

But before we dive into this week’s coverage, we would like to draw our readers’ attention to a special report issued by The Risk Protocol, a specialized investment platform that provides research and insights focused on measuring and managing risk within digital asset markets. Their report covers a wide gamut of cryptoassets, and dives into quantitative analysis of volatility. It breaks down correlation between crypto assets, as well as with the broader market, and discusses the leverage and calendar effects in returns and volatility.

Similarly, we would like to present our latest research report, describing the function of the Uniswap V2 decentralized exchange. This research walks through the inner mechanisms of the automated market maker (AMM) exchange design, as well as the smart contract logic underlying token pair swaps.

The Need for Liquid Staking Derivatives

At a fundamental level, staking refers to the process of leveraging digital assets to secure a proof-of-stake (PoS) network. Users can choose to commit the assets themselves (“solo staking”) or contribute to staking pools. Each option carries a set of trade offs. Solo staking involves running an Ethereum Node and requires depositing 32 ETH (~$57K) to activate a validator. In an ideal world, many participants would solo stake to achieve the best network decentralization. However, the current presence of financial, technical, and operational hurdles make this less of a reality for most. As a solution to these hurdles, Liquid Staking Derivatives have emerged as a widely adopted choice.

To bypass the 32 ETH requirement, staking pools are an alternative that aggregate user funds, allowing stakers to participate with fewer than 32 ETH. Operational aspects of staking, on the other hand, are handled by node operators, which are entities managing validator infrastructure. Most importantly, users are issued a tokenized derivative in exchange for their staked ETH. In other words, the token represents a claim on the underlying stake pool and its yield in the form of a receipt that can be traded across centralized and decentralized applications.

Simply put, liquid staking allows users to secure the Ethereum network and participate in on-chain activities while simultaneously earning staking yields.

As a result of these benefits, the current supply of ETH staked has reached ~17.5M, representing approximately 15% of ETH supply.

Source: Coin Metrics’ Network Data

Liquid Staking Industry Landscape

The landscape of liquid staking derivatives is diverse, with several market participants offering varying token models and validator selection processes. The choice of staking derivative has implications for the user's impact on the protocol and determines where these derivatives lie on the decentralization spectrum. By focusing on the major liquid staking protocols in use today, we can gain insight into how each solution compares to solo staking and how they stack up against one another.

Lido stETH

Lido is a non-custodial liquid staking protocol, and is the current market leader, propelled by its first-mover advantage. To date, Lido’s staking pools have ~5.5M ETH deposited, representing a 30% share of total ETH staked on the Beacon Chain . When a user deposits ETH via Lido’s smart contract, funds are pooled between node operators and then distributed to a curated set of validators. Hence, the Lido protocol can be thought of as a glue layer that connects pooled capital to node operators.

Users receive ‘stETH’ (staked ETH), a liquid staking token minted at a 1:1 ratio to the assets deposited. stETH follows a ‘rebasing’ mechanism by which its balance adjusts daily to reflect the value of the initial deposit plus staking yields. For a user, this translates to the automatic rebalancing of stETH without the need for accompanying transactions.

Source: Coin Metrics’ Network Data

stETH in DeFi

The rebasing token model facilitates a user-friendly experience, but isn’t compatible with liquidity pool based protocols such as Uniswap (due to constant supply changes in stETH and ERC-20 incompatibility, leading to the wstETH token). Despite this, Lido’s stETH allows users to stake their ETH and simultaneously use the liquid staking token to leverage yield opportunities across DeFi applications. For example, depositing the receipt token as collateral in lending applications such as Aave or Compound. This simple idea has led to liquid staking tokens becoming the base asset for several use cases in DeFi. Using Aave v2 lending markets as a proxy, a rise in the popularity of stETH is evident with its share of TVL (total value locked) rising to 42%. In general, growing integrations with DeFi protocols can expand the staking tokens liquidity with the creation of secondary markets.

Source: Coin Metrics Labs DeFi Balance Sheets

Another crucial metric is the discount/premium of the liquid staking token to its underlying asset. In the case of Lido, the divergence between stETH and ETH reflects liquidity, smart-contract and collateral risks. For instance, if the market perceives that Lido’s smart contract cannot deliver the underlying ETH, the derivative would trade at a discount. Cases of stETH massively decoupling from its intended peg have been observed—such as the liquidity crunch in May–June 2022, when Celsius and Three Arrows Capital withdrew large amounts of stETH from the Curve Finance liquidity pool. However, the stETH peg has seen a period of stability lately as a result of renewed confidence around liquidity with the Shanghai hard fork approaching.

Coinbase cbETH

Coinbase is a prominent centralized exchange which offers custodial liquid staking through the issuance of its liquid staking token, Coinbase Wrapped Staked ETH (cbETH). With Lido’s stETH being widely adopted, and close to reaching 33% network penetration, Coinbase provides an alternative to further diversify underlying stake on the Ethereum network. The cbETH token follows a similar approach to the cToken model adopted by Compound. As opposed to a rebasing token used by Lido, cbETH is issued/redeemed based on a floating exchange rate. In other words, a user's cbETH balance does not increase as staking rewards are earned instead representing the principal amount (ETH Staked) + staking rewards accrued – penalties (slashings). This exchange rate is then applied when a user “unwraps” their staked ETH. Therefore, 1 cbETH does not necessarily represent 1 staked ETH. This ERC-20 compatible token model in addition to Coinbase’s trusted brand, convenience, and regulatory safety has resulted in cbETH being the second most-adopted liquid staking derivative. cbETH has also garnered several integrations with DeFi protocols, such as Uniswap, Curve, Aave and Compound to further fuel its usage.

The adoption of cbETH is evident through the chart above, which displays the cumulative supply of cbETH issued – redeemed. With its first issuance in June 2022, representing a 1:1 ratio of staked ETH and cbETH, its supply has since risen to 1.14M as of March 2023. Traders can find these tokens on exchanges, including Coinbase and Uniswap, where they can purchase cbETH at a discount. Daily cbETH-USD trading volume on Coinbase has typically ranged between $4–6M, with close to $10M during days with increased volatility seen in September and early November. Volumes on Uniswap V3 have experienced a significant uptick through the start of 2023, and reached $31M in trading volume on March 13th, as traders took advantage of a discount during the volatile period.

Source: Coin Metrics’ Market Data Feed

The cbETH premium/discount also highlights the unique risks associated with the liquid staking token in addition to its token model. With cbETH being a product of a centralized exchange in Coinbase, counterparty risks in addition to the need for KYC and complexity in redeeming play a more important role. This dynamic has been reflected in the cbETH peg trading at a significant discount since its inception, but closing the gap as we approach the Shanghai upgrade.

Source: Coin Metrics Pro Charts

Rocketpool rETH

Created in November 2021, Rocket Pool entered the liquid staking ecosystem touted to be most aligned with the principles of the Ethereum network. Underpinned by the rETH token, Rocket Pool has facilitated ~435,000 in ETH staked, and is currently 3rd by market share compared to Coinbase and Lido. As highlighted earlier, solo stakers are required to deploy assets in multiples of 32 ETH. Rocket Pool, on the other hand, functions with “minipools,” halving the requirement of 16 ETH per validator. This is combined with an additional 16 ETH from the deposit pool to create the same conditions as a regular validator on the Beacon Chain. Users receive rETH from the pooled capital in exchange for depositing any amount of their ETH through Rocket Pool. rETH’s follows a reward-bearing model like the cToken model adopted by Coinbase. Its balance, therefore, is not elastic and results in the ratio of rETH and ETH to increase over time.

Risks of Liquid Staking Derivatives

Despite several benefits such as lower barriers to staking, increased network security, capital efficiency, liquid staking derivatives also pose significant risks to the Ethereum network. As stated by Ethereum Foundation researcher Danny Ryan, liquid staking can have a tendency towards centralization through “cartelization.” This is due to a dynamic where the most popular liquid staking platforms attract the most capital, thereby increasing their underlying stake and utility creating a virtuous cycle that leads to centralization. Therefore, if a liquid staking protocol exceeds certain thresholds (i.e., by controlling greater than ⅓ or ½ of pooled capital) it can result in undesirable outcomes such as censorship, coordination in MEV extraction, and other forms of manipulation. Governance can also create an additional layer of risk as token-holders of these platforms can influence choices made within the system (e.g., selection of node operators) to favor increased returns at the detriment of the Ethereum network as a whole. Additionally, the custodial nature of certain solutions can introduce counterparty risk by not being able to meet obligations. The recent regulatory scrutiny of Kraken’s staking-as-a-service platform has also spurred conversation around the potential ramifications on other such staking providers.

Conclusion

Staking has become a crucial component of the digital asset industry, offering users the opportunity to earn a native yield by helping secure PoS blockchains without assuming credit risk. A plethora of new solutions, infrastructure upgrades, and exciting primitives have emerged to meet the demand for staking. To name a few entrants, Frax Finance is a platform that enables higher yields on staked ETH through a two-token model. Liquid Collective, on the other hand, is an enterprise-grade liquid staking solution backed by a diverse group of operators, catered towards institutional stakers. Meanwhile, incumbents like Lido are introducing core infrastructure upgrades such as Lido V2, which will allow the onboarding of distinct validator sets via a modular architecture. Emerging technologies in the form of distributed validator technology (DVT) and Eigenlayer’s re-staking also bring improvements in validator performance and the ability to extend Ethereum's security beyond the network itself. With the Shanghai hard fork on the horizon, there is no shortage of exciting developments to keep us on our toes.

Network Data Insights

Summary Metrics

Source: Coin Metrics Network Data Pro

The Market caps of BTC and ETH experienced a rapid reversal with a 21% and 14% rise respectively on the back of a strong week for digital asset markets. Active addresses on Tether (ETH) rose by 12% whereas USDC saw 35% decline in active users a week after increased activity due its de-peg.

Coin Metrics Updates

This week’s updates from the Coin Metrics team:

For the best in-depth discussion of CM data and research, come check out our research community on the web3 social media platform gm.xyz.

As always, if you have any feedback or requests please let us know here.

Subscribe and Past Issues

Coin Metrics’ State of the Network, is an unbiased, weekly view of the crypto market informed by our own network (on-chain) and market data.

If you'd like to get State of the Network in your inbox, please subscribe here. You can see previous issues of State of the Network here.