State of the Network’s 2024 Year in Review

A data-driven overview of events that shaped crypto in 2024

Get the best data-driven crypto insights and analysis every week:

State of the Network’s 2024 Year in Review

By: Tanay Ved

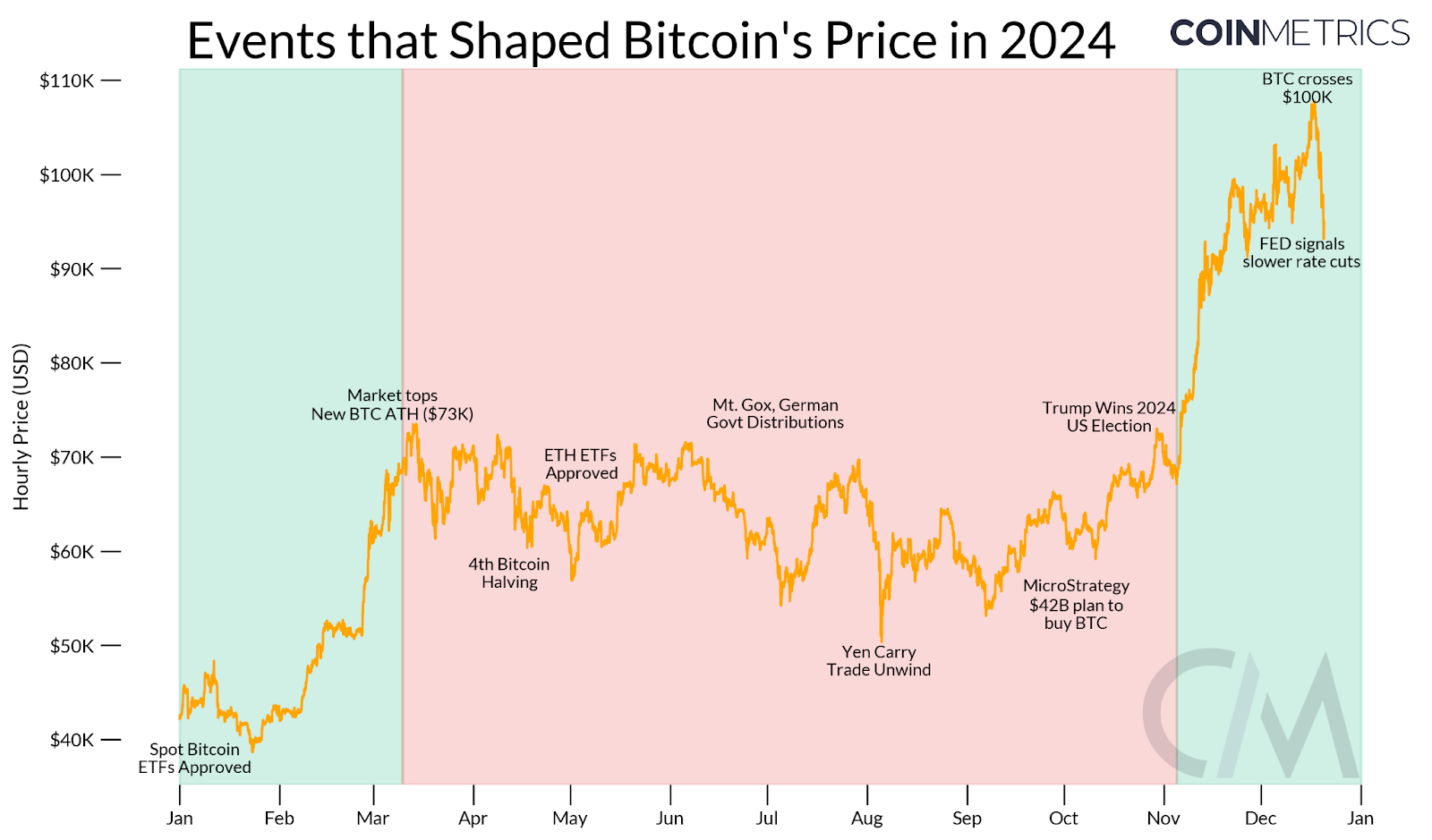

As we wrap up 2024, a year that stands in stark contrast to the crypto winter of 2022, we’d like to pause and reminisce on a momentous year for the crypto industry. 2024 was one of the most consequential years in the history of crypto across multiple fronts, starting with the launch of Bitcoin ETFs and concluding with Bitcoin crossing $100K post- election. In this special issue of Coin Metrics’ State of the Network, we revisit the major developments that shaped the digital assets industry in 2024 through a data-driven lens.

Source: Coin Metrics Reference Rates, Intraday

Propelled by the explosive success of Bitcoin ETFs in January, the crypto market saw a strong phase of growth in Q1 with Bitcoin soaring to new all-time highs of $73K. What followed was a quieter period of consolidation, characterized by subdued catalysts and significant supply redistributions from major market participants. Now, as 2024 draws to a close, optimism has returned, fueled by a pro-crypto U.S. administration and the onset of a rate-cutting cycle.

Source: Coin Metrics Reference Rates, datonomyTM (As of Monday December 23rd)

Bitcoin (BTC) undeniably took center stage this year, outperforming traditional asset classes and crypto-assets with a 125% gain year-to-date. Solana (SOL) led the market several times this cycle, ending the year 78% higher, while Ethereum’s (ETH) continued its relative underperformance, rising 44% over the year.

The chart above illustrates the top 30 cryptoassets in the datonomyTM universe, with a market capitalization of over $1 Billion. Memecoins like DOGE and PEPE captured widespread attention fueled by retail exuberance, while “Dino coins” such as Ripple (XRP) and Stellar (XLM) staged an unexpected comeback. Alternative Layer-1s like Sui (SUI) and established blue-chip DeFi protocols like Aave also gained traction, reflecting the investor sentiment and thematic rotations that shaped the market in 2024.

Q1: ETF Floodgates Open, Memecoin Mania & Ethereum Scales with Blobs

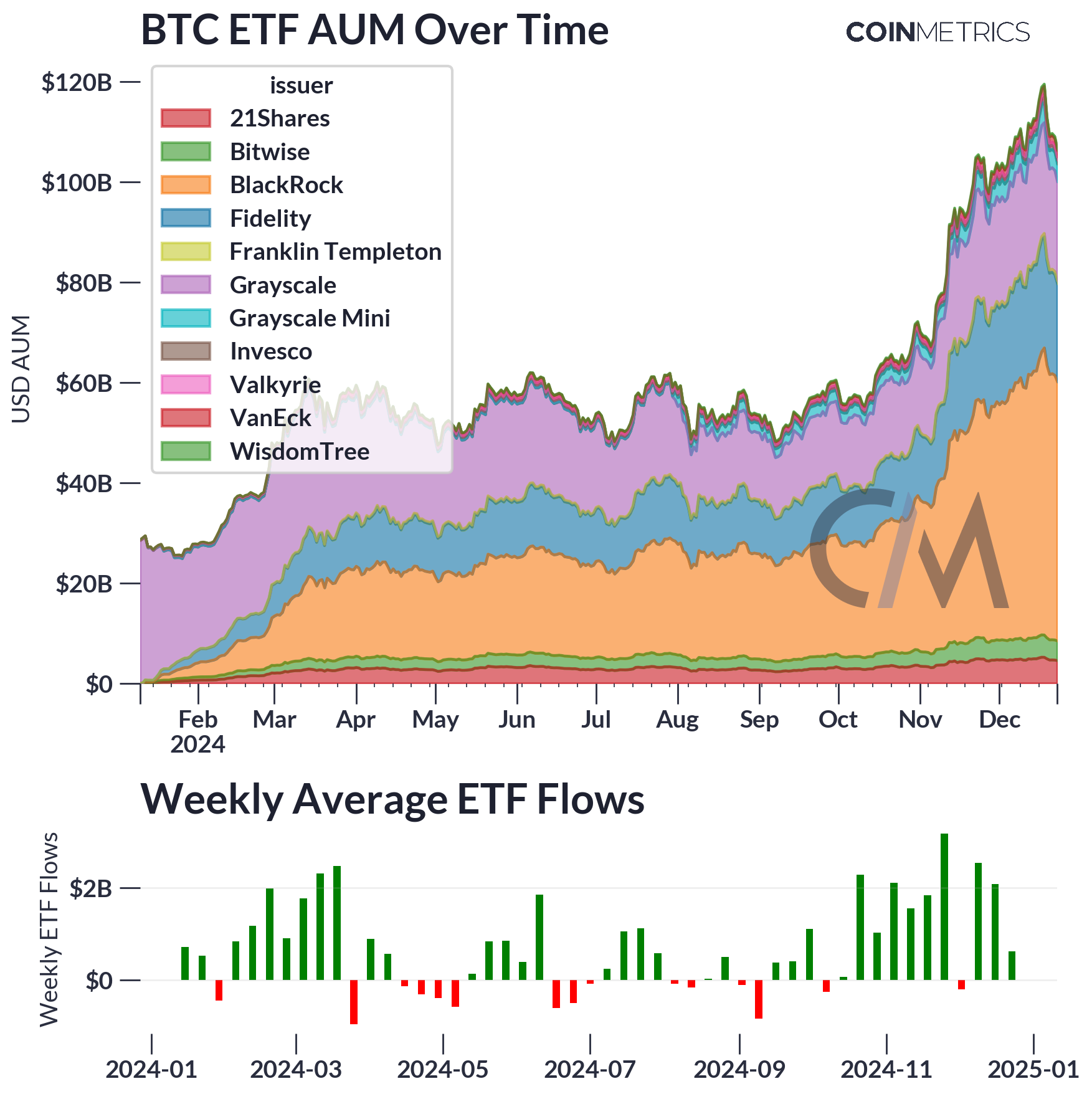

The arrival of spot Bitcoin ETFs ushered in a large wave of adoption and opened the floodgates to Wall Street. Assets under management (AUM) for the 11 issuers now exceeds $105B, with over 1.2M bitcoin held by the vehicles. This amounts to 5.6% of Bitcoin’s current supply with demand from corporate balance sheets further accelerating the pace at which supply is absorbed. In less than a year since their launch, spot Bitcoin ETFs have experienced robust flows, cementing their position as the most successful debut of any ETF category in history.

Weekly flows illustrate consistent accumulation, with peak weeks exceeding $2B in net additions, although occasional outflows were observed during market consolidations in the summer months.

Source: Coin Metrics Labs

In parallel to this Bitcoin driven institutional adoption that pushed the overall market higher, memecoins started to attract tremendous mindshare, leading to an uptrend driven by extreme ends of the risk spectrum. In early March, spot trading volume for meme coins hit $13B, as the market capitalization of major meme coins reached $60B.

Source: Coin Metrics Market Data Feed

While established, large-cap memecoins saw a boost, a majority of activity stemmed from a big bang of newly launched meme coins on Solana. A platform called pump.fun became the epicenter of the memecoin explosion in Q1, facilitating the creation of over 75,000 tokens and pushed active wallets on Solana to a then-record high of 2.06M. While these high levels of activity did not sustain, meme coins made a comeback, with volumes eclipsing $23B in November. New AI-agent platforms like Virtuals on Base have injected fresh energy into this phenomenon.

Source: Coin Metrics Network Data Pro

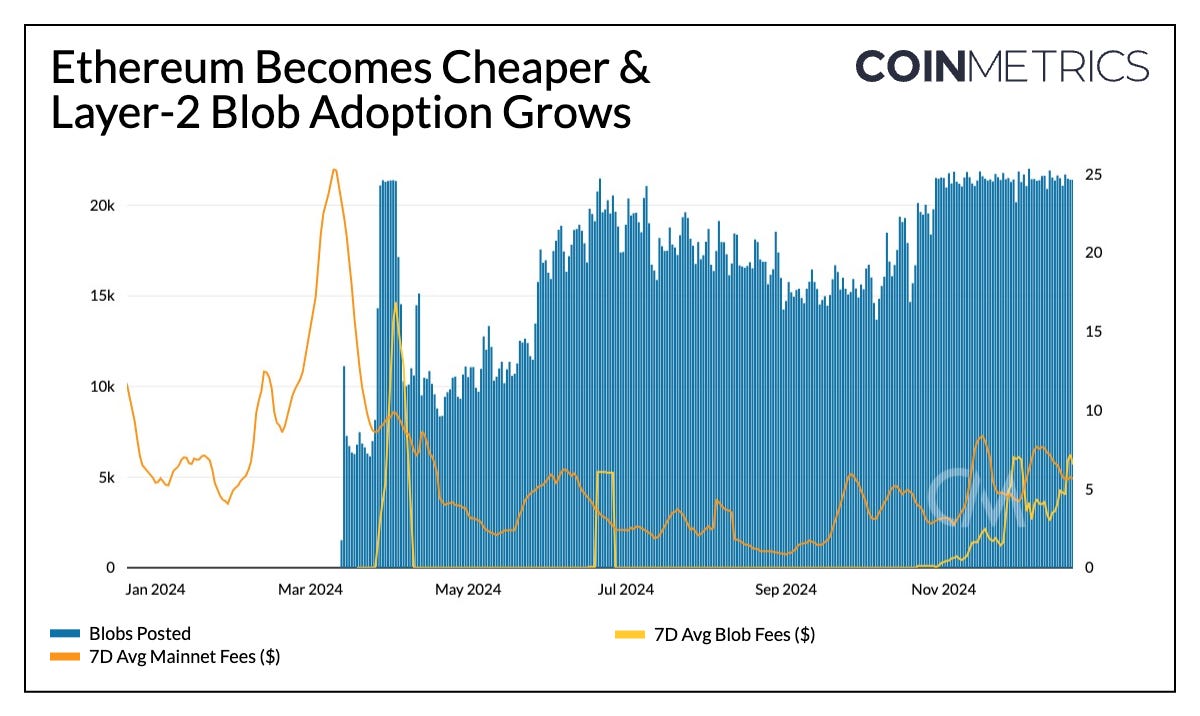

March also marked a major milestone for Ethereum with the deployment of EIP-4844 as part of the Dencun upgrade. Soon after, Ethereum Layer-2 rollups adopted a new fee market for blob transactions in parallel to mainnet. This laid the foundation for Ethereum to scale execution with the help of Layer-2s like Base, Optimism and Arbitrum while reducing the cost of settlement to the Layer-1, making transacting on the network more affordable. Demand for blobs has been robust, with Ethereum consistently hitting its target capacity of three blobs per block just seven months after launch.

While this has made the Ethereum ecosystem more accessible, it has arguably hindered ETH’s value accrual due to reduced Layer-1 fees, while also contributing to a more fragmented user experience. However, there are no signs of exhaustion in the space, with Layer-2s being spun up by prominent exchanges in Kraken & Uniswap, Deutsche Bank and a multinational conglomerate (Sony), with increases in blob capacity on the horizon.

Q2: Sideways Summer: A Season of Supply Unlocks

Q2 was characterized by a period of consolidation, where the market found itself rangebound driven by a lack of catalysts. In April, Bitcoin underwent its quadrennial halving event, reducing BTC’s daily issuance from 900 to 450 BTC. As is typical with halvings, this presented an inflection point for the mining industry, forcing miners to adapt to the diminished block subsidies. The event spurred upgrades to more efficient ASIC hardware, triggered further consolidation in the mining sector, and prompted some miners to repurpose their infrastructure for AI data centers to diversify revenue streams.

As shown in the chart below, transaction fees became a key component of mining revenue, partially offsetting declining block subsidies. Despite this, the overall hashprice (daily USD revenue per TH/s) remained under pressure, reflecting miners' growing reliance on network activity for sustainability.

Source: Coin Metrics Network Data Pro

Compounding these challenges were additional supply pressures. One of the most notable was the long-awaited distribution of assets from the Mt. Gox bankruptcy, which saw thousands of BTC re-enter the market. Similarly, the German government’s sale of over 50,000 BTC seized in criminal investigations added to the selling pressure, exacerbating supply-side dynamics. Despite this confluence of sales, Bitcoin's liquidity proved resilient, absorbing the supply without major disruptions to market stability. Looking ahead, selling pressures may ease as FTX creditors are set to receive cash distributions in 2025 that could re-enter the market.

Q3: Stablecoin & Tokenization Spring

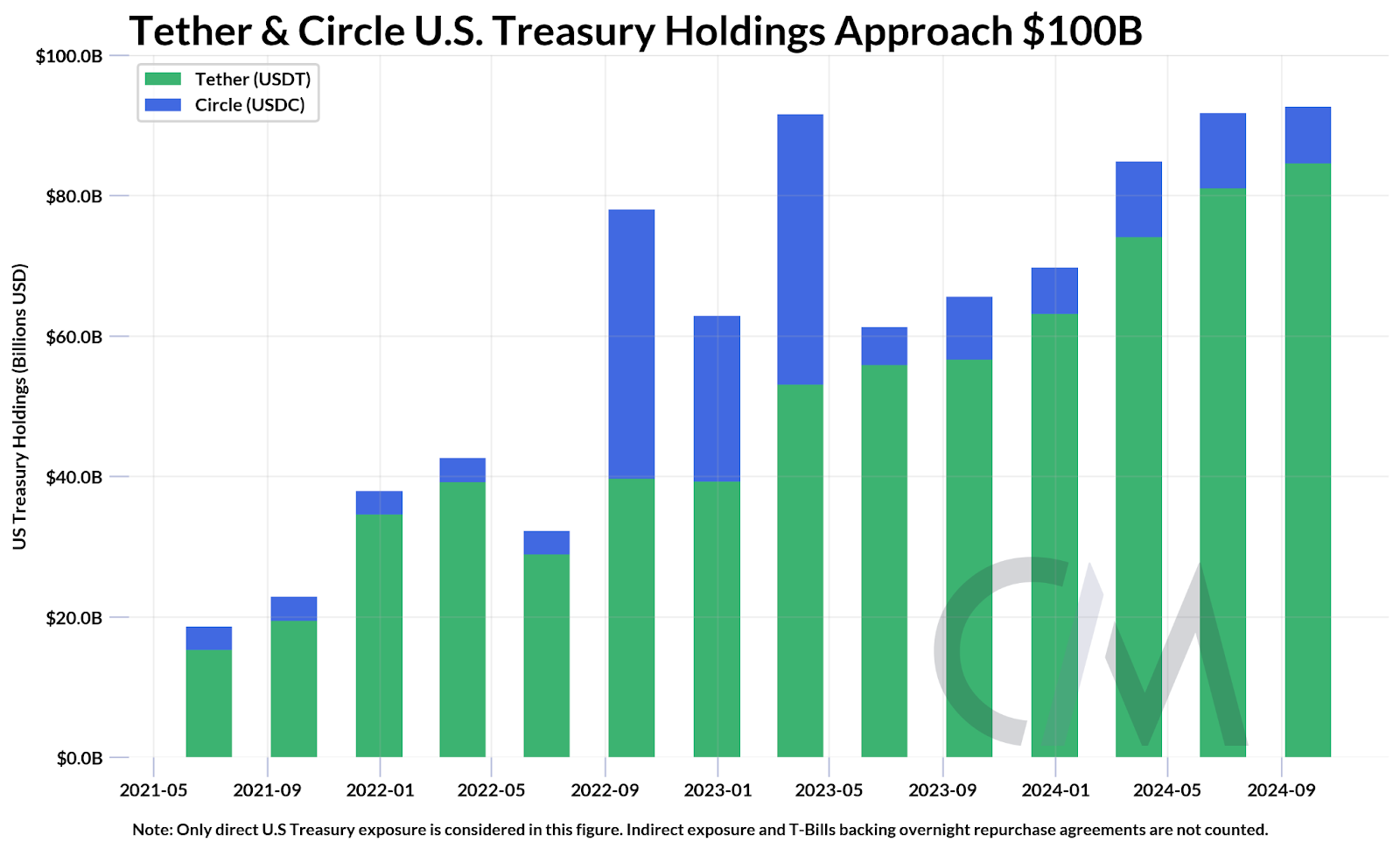

Ubiquitously recognized as "crypto's killer app”, the global importance of stablecoins started permeating beyond the crypto industry. Stablecoins continued to export the dollar around the world, crossing an aggregate $210B in supply. USDT ($138B) and USDC ($42B) remained the dominant players, while a majority of stablecoin supply tilted in favor of the Ethereum network, with $122B in stablecoin supply. Altogether, stablecoins facilitated $1.4T in monthly (adjusted) transfer volumes in November.

While stablecoins’ role as a medium of exchange and store of value in emerging economies has been widely explored, momentum around their utility in payments and financial services infrastructure accelerated with Stripe’s acquisition of Bridge. Furthermore, with 99% of stablecoins USD-pegged and nearly $100B directly invested in U.S. Treasuries by Tether and Circle, they also solidified their position as key vehicles for preserving dollar dominance on a global scale.

Source: Tether & Circle Attestations

In parallel, BlackRock entered the tokenization space, launching the BlackRock USD Institutional Digital Liquidity Fund (BUIDL), investing in dollar-equivalent assets like cash and US Treasury bills. BUIDL quickly reached a supply of 500M, growing the landscape of tokenized securities on public blockchains. The ecosystem expanded in 2024, offering stablecoins with varying risk profiles, liquidity, collateral and savings mechanisms. Ethena's USDe stood out, growing from $91M to $6B in market capitalization to become the third-largest stablecoin by leveraging positive funding rates during market uptrends to deliver attractive yields to holders. Meanwhile, First Digital USD (FDUSD) gained prominence as a source of liquidity and widely used quote currency on exchanges.

Regulatory focus on stablecoins intensified, reflecting their growing importance in the global financial system. The European Union implemented stablecoin-specific requirements under the Markets in Crypto-Assets (MiCA) regulation, which has begun to reshape the Euro-pegged stablecoin sector.

Source: Coin Metrics Network Data Pro

Q4: Election Euphoria

The 2024 U.S. presidential election had a profound impact on digital asset markets, propelling BTC above $100K for the first time. Specialized Coins (including meme & privacy coins) and Smart Contract Platforms in Coin Metrics’ datonomyTM universe were standout sectors, returning 129% and 84% since the election, respectively.

Source: Coin Metrics datonomyTM

Leading up to the election, we also witnessed the rise of prediction markets like Polymarket, which played a pivotal role in capturing the collective intelligence for electoral outcomes. At its peak, Polymarket crossed an open interest of $450 million. While activity on the platform has now subsided, it showcased the utility and potential for information markets on public blockchains.

Market optimism surged post-election, fueled by the administration’s pro-crypto stance, a stark departure from the regulatory headwinds of the prior SEC regime. Demand from ETFs and corporate treasuries bolstered the rally, with MicroStrategy’s holdings reaching 444,262 BTC, funded by its equity and convertible bond offerings. Institutional interest hit new highs in derivatives markets, as reflected in record Bitcoin futures open interest of $22.7B on CME out of a total of $52B+, alongside the launch of options-based ETFs.

Source: Coin Metrics Market Data Feed

Despite this momentum, uncertainties remain regarding the implementation and timeline of crypto-friendly policies. While there are clear indications of a shift towards a more supportive regulatory environment, including the appointment of crypto advocates to key positions like SEC chair and crypto czar, specific regulatory frameworks remain unclear. Market exuberance has also been tempered by revised expectations for interest rate cuts, leaving participants cautiously optimistic heading into 2025.

Nevertheless, 2024 leaves us with a strong foundation: the introduction of spot Bitcoin ETFs, acceleration of stablecoin adoption, significant strides in on-chain infrastructure and applications, and a pro-crypto administration taking office at the onset of a rate-cutting cycle. As we transition into the next year, stay tuned for our 2025 Crypto Outlook report, where we’ll explore key themes and trends shaping the year ahead.

Coin Metrics Research in 2024

Reports:

Dashboards:

Find our weekly State of the Network (SOTN) & State of the Market (SOTM) newsletters on our insights page. As always, if you have any feedback or requests please let us know here.

Subscribe and Past Issues

Coin Metrics’ State of the Network, is an unbiased, weekly view of the crypto market informed by our own network (on-chain) and market data.

If you'd like to get State of the Network in your inbox, please subscribe here. You can see previous issues of State of the Network here.