Coin Metrics' State of the Network: Issue 17

Tuesday, September 17, 2019

Weekly Feature

ETH is Overtaking BTC in Daily Transaction Fees, Driven by Tether

ETH is on the verge of overtaking BTC in daily transaction fees. As of September 15th, ETH had $182,899 daily transaction fees compared to $185,993 for BTC:

ETH has overtaken BTC’s daily transaction fees several times before over the course of 2019. The below chart shows the ratio of BTC daily fees to ETH’s daily fees (i.e. BTC Fees/ETH Fees), both in USD.

If BTC’s fees are higher than ETH’s, the ratio is above 1, while if BTC’s fees are lower than ETH’s the ratio is below 1. For example, ETH’s daily transaction fees surpassed BTC’s daily fees on February 19th, 2019 and March 18th, 2019. This causes the BTC/ETH fees line to dip below 1 on both of those dates in the below chart.

Thank you to Spencer Noon for tweeting about this and inspiring the following charts:

There has been debate in the past about whether highs fees are detrimental to a crypto network. But ultimately, transaction fees represent real network demand and usage. Importantly, high fees are critical to long term network security. When block rewards decrease over time, fees become a larger and larger percentage of total miner revenue. Total fees therefore are a strong signal of overall network health and long-term sustainability.

The below chart shows BTC/ETH fees ratio from the beginning of 2018 onward (we omitted prior data because BTC fees were consistently at least 10-25x ETH’s before 2018). There were brief periods in 2018 when ETH had more daily transaction fees than BTC, but for the most part BTC has been on top. In fact, from early April to mid August 2019 BTC’s daily transaction fees surged ahead of ETH’s, mostly remaining 5-10x ETH’s over the four month stretch:

But over the last thirty days, BTC’s fees have come crashing down while ETH’s have shot up. There are probably many factors involved in this recent swing. However there is one big recent change that has likely played a major role in driving the latest fee reversal: Tether’s migration from the Bitcoin based Omni protocol to Ethereum.

Tether (USDT) was initially built on the Omni protocol, which is built on top of the Bitcoin blockchain. But Tether now also supports a version of their token on the Ethereum protocol (USDT-ETH). Over the course of 2019, Tether users has been migrating from the Omni version of Tether to the Ethereum version. Despite the change, Tether is still by far the most dominant stablecoin, as we covered in State of the Network Issue 15.

USDT on OMNI was growing over most of the course of 2019. In fact, USDT transaction count even began hitting new all-time highs starting around April, 2019, peaking at 91,513 on August 7th.

But since then, USDT-ETH has skyrocketed. The Ethereum version of Tether hit a new all-time high of 187,912 daily transactions on September 9th. USDT-ETH is generating so many transactions that it recently accounted for over 25% of all Ethereum transactions on September 8th, and has consistently accounted for more than 10% of all Ethereum transactions since mid August:

Similarly, USDT-ETH also recently vaulted past USDT (Omni) in daily adjusted transfer value after USDT (Omni) reached transfer value all-time highs. The below chart shows adjusted transfer value smoothed using a seven day rolling average.

Addresses with balances of at least $10 show a similar pattern. The below chart shows the number of unique addresses holding at least $10 on USDT (Omni) and USDT-ETH. We typically use addresses with at least $10 to approximate users since it is small enough to potentially represent a retail investor (as opposed to an institution) but large enough to be a non-dust account (however this is only a proxy - in reality, many users have more than one address). The Ethereum version is now about even with the Omni version, after the Omni version surged to all-time highs, peaking in July.

Ethereum total daily gas also recently reached an all-time high, likely due to USDT-ETH’s recent surge. According to ETH Gas Station, Tether is the biggest gas spender out of all Ethereum contracts over the last 30 days.

Lastly, the below chart shows ETH and BTC fees as a percentage of total miner revenue (i.e. fees + block rewards). ETH has started to climb ahead of BTC over the last 30 days.

All of this suggests that the recent ETH/BTC fee flip is likely being driven by the switch from USDT (Omni) to USDT-ETH. If this is the case, the fee flip could continue to grow moving forward as more users switch from over to the Ethereum version of the protocol. We will continue to monitor this and provide updates in future version of State of the Network.

Network Data Insights

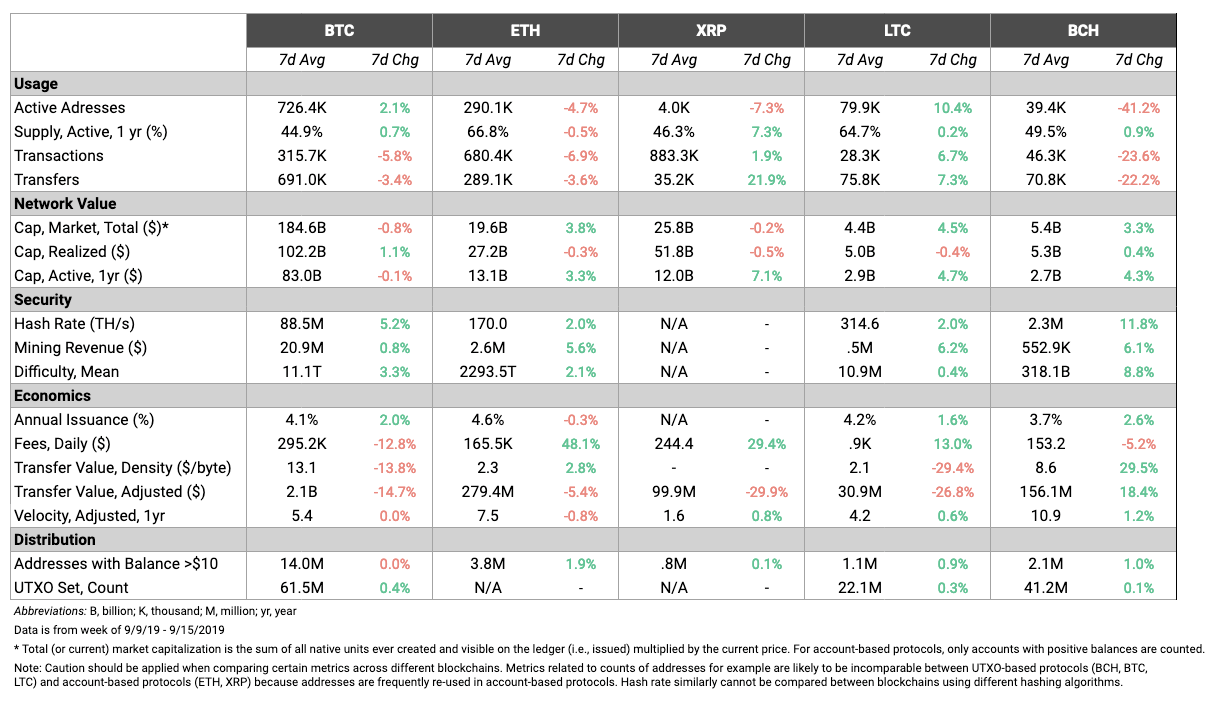

Summary Metrics

Crypto networks were relatively stable over the last week, outside of a few metrics. As noted in this week’s weekly feature, BTC’s fees dropped by over 12% this past week, while ETH’s fees grew by 48.1%. BTC and ETH’s hash rate and difficulty both increased, however, which is a positive signal for overall network security.

BCH, on the other hand, had a relatively volatile week. While adjusted transfer value grew by 18.4% week over week, BCH transaction count dropped by 23.6%. Similar to BTC, BCH’s fees dropped, while the hash rate and difficulty grew significantly.

Network Highlights

ZEC is approaching $1 billion cumulative mining revenue (aka thermocap). As of September 15th, ZEC has generated $994,842,737 of total mining revenue.

BCH supply recently surpassed 18,000,000. BCH passed the milestone on September 13th. Comparatively, BTC’s supply was 17,934,192 on September 13th. BCH is currently on pace to hit its next block reward halving sooner than BTC. BCH is expected to hit its next halving on April 8th, 2020, while BTC’s next halving is expected on May 15th, 2020.

Market Data Insights

Limited Response to Global Events from Bitcoin This Week

Earlier this year, the narrative that Bitcoin serves as a store-of-value and haven asset in times of increased geopolitical risk was supported by empirical data as both Bitcoin and gold (along with other traditional haven assets) rose in price.

In theory, the intrinsic qualities of Bitcoin support this narrative -- under market environments in which geopolitical or financial instability is increasing (more than what’s priced in), the need for store-of-value assets that are immune from policy errors increase. Moreover, we should also expect to see an inverse relationship in Bitcoin’s price to changes in real yields. As nominal interest rates decline, the opportunity cost for holding a non-yield producing asset like Bitcoin declines. And as inflation rises, the need for wealth-preserving qualities of Bitcoin grows.

The problem with this narrative is the inconsistent empirical data. This week, two significant events impacted major financial markets: the European Central Bank’s announcement of monetary policy easing by cutting a key interest rate and restarting its quantitative easing program, and an attack on one of Saudi Arabia’s key oil processing facilities which led to the largest sudden supply disruption in history. Despite major moves in certain financial markets, including a 20 percent change in oil prices and a corresponding bid in haven assets, Bitcoin remained nearly unchanged. This indicates that previous examples of safe haven behavior are spurious in nature or that its reaction function to geopolitical and macroeconomic events is still not fully understood.

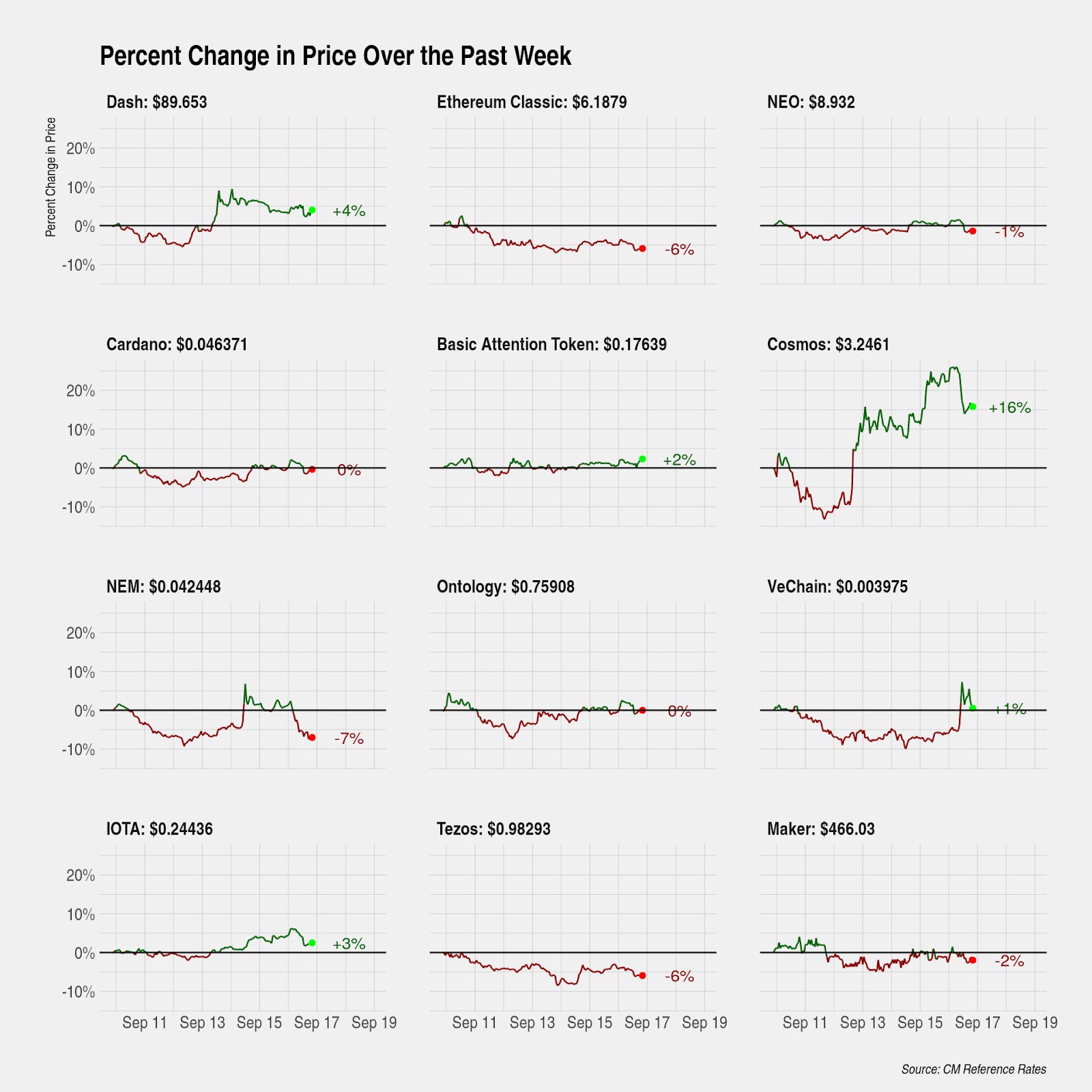

Strong Weekly Performance for Ethereum and Cosmos

Ethereum (+6%) saw gains this week marking the second week in a row in which Ethereum was a notable outperformer. This has moderated the strong long-term trend of Bitcoin outperformance that has been in place since the peak of the previous market cycle. Cosmos (+16%) also experienced strong gains this week.

CM Bletchley Indexes (CMBI) Insights

This week all Bletchley Indexes experienced minor losses after a week characterized by low volatility across the market. The Bletchley 20 and Bletchley 40 continued to fall against Bitcoin, still printing new lows on a weekly basis. This trend has persisted since early 2018 but over the last month has recently flattened out, potentially indicating some strength for mid and small cap assets.

Coin Metrics Updates

This week’s updates from the Coin Metrics team:

Coin Metrics is hiring! We recently opened up 7 new roles, including Blockchain Data Engineer and Data Quality and Operations Lead. Please check out our Careers page to view the openings.

As always, if you have any feedback or requests, don’t hesitate to reach out at info@coinmetrics.io.

Subscribe and Past Issues

Coin Metrics’ State of the Network, is an unbiased, weekly view of the crypto market informed by our own network (on-chain) and market data.

If you'd like to get State of the Network in your inbox, please subscribe here. You can see previous issues of State of the Network here.

Check out the Coin Metrics Blog for more in depth research and analysis.