Coin Metrics' State of the Network: Issue 129

Tuesday, November 16th, 2021

Get the best data-driven crypto insights and analysis every week:

Bitcoin & CPI Hit New Highs

By Nate Maddrey and Kyle Waters

Bitcoin price jumped to a new all-time high of $68,998 on November 10th after Consumer Price Index (CPI) data showed inflation to be at a 30 year high. Price began to climb shortly after 8:30 AM EST (13:30 UTC) when the news was initially released. The price spike was short-lived, however - BTC fell back down below $65K amidst a wider selloff as the stock market dropped in response to the news.

Source: Coin Metrics Reference Rates

Bitcoin’s correlation with equities has been increasing over the past few months (after falling to close to 0 earlier in 2021) as bitcoin increasingly responds to news from the Fed and other policy markers. The following chart shows BTC’s 90-day rolling correlation with S&P 500 (SPY) as a proxy for the stock market. Historically, BTC has been mostly uncorrelated with the S&P 500. The correlation jumped to an all-time high in 2020 following the global onset of COVID-19, but never grew particularly strong - at its peak it was 0.48.

Source: Coin Metrics Correlation Charts

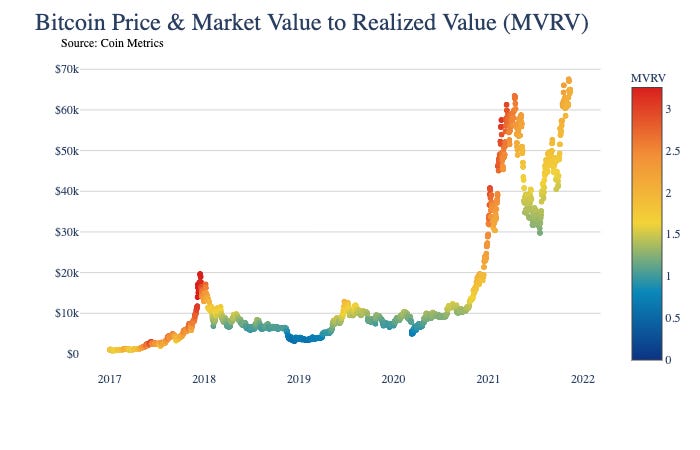

Even though BTC is breaking new all-time highs, its free float market value to realized value (MVRV) ratio is currently relatively low. Market value to realized value (MVRV) has historically been one of the most reliable on-chain indicators of bitcoin market tops and bottoms. During previous cycles a free float MVRV of 3.0 or above has indicated a local top, while an MVRV of below 1.0 has indicated the bottom of the cycle. Free float MVRV is currently about 2.1. For more information about MVRV and an in-depth explanation of how it's calculated check out our On-Chain Indicators Primer.

Source: Coin Metrics Network Data Pro

Ethereum Name Service Launches $ENS Token

Last week, Ethereum Name Service (ENS) launched its $ENS governance token as part of a broader push to decentralize ownership of the protocol via the creation of a DAO and token. ENS is an open-source naming system that allows users to map human-readable names to hard-to-remember crypto identifiers such as a 42-character hexadecimal public Ethereum address (0x000…).

Like many protocols that have launched tokens, a portion of the token supply was given to early adopters via an airdrop. While $ENS is by no means the first protocol to allocate a percentage of tokens to users via an airdrop, the specific economics around the $ENS token are interesting because unlike many other projects, ENS never received any outside investment or funding. Twenty-five million or one quarter of all $ENS tokens were airdropped to the ~137K eligible addresses holding a .ETH name.

Although eligible addresses have until next May to claim, many addresses have quickly moved to claim their tokens despite the recent rise in gas prices on Ethereum. Out of the 25M $ENS tokens airdropped to the community, ~15.6M have been claimed (~62%) as of 2pm ET on November 15th. Of the roughly 137K total eligible addresses, about 80.2K (~58.5%) have claimed their $ENS thus far.

Each eligible address received an amount of $ENS tokens proportional to the number of days owning at least one ENS name and the number of days until the expiration of the last name on the account. From an incentives standpoint, early adopters and more involved users are thought to be more invested in the future of the protocol and therefore should receive more voting power. Interestingly, the allocation formula did not directly take into account the number of ENS names held by an address, likely to emphasize ENS users over ENS name “collectors”.

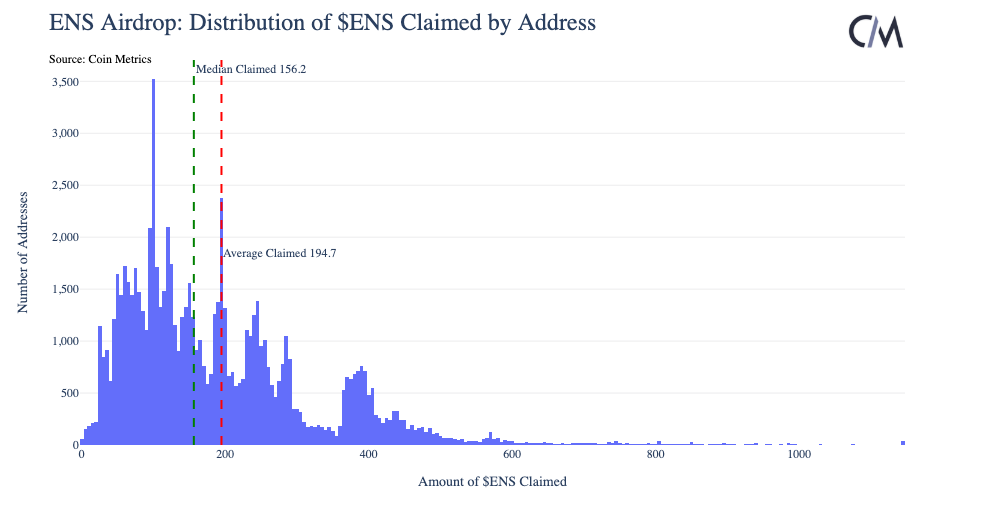

The histograms below show the distribution of $ENS claimed so far by address in native units and in USD (at a price of $50/token). The average address has claimed 194.7 tokens valued at $9,248 at a price of $50. A total of 40 addresses have received the max 1,143 $ENS (a cap was added to the formula because some addresses have registered ENS names out thousands of years, the current longest being until the year 4271).

The ENS airdrop was one of the largest on Ethereum to-date ranking amongst the now famous launch of Uniswap’s governance token UNI in September 2020. In the retroactive UNI airdrop, any address that had ever called Uniswap v1 or v2 contracts (~250K addresses) was given 400 UNI, now worth ~$10K.

Front End to Popular Tezos NFT Platform Hic et Nunc (HEN) Unexpectedly “Discontinued”

Last Thursday, the main front end to the Tezos-based NFT platform Hic et Nunc (HEN) unexpectedly went down while the official Twitter account for the platform simply read “discontinued.” After the dust settled, it became clear that the creator of the platform suddenly decided to walk away from the project, shutting down the website in the process.

This was a surprising move to a growing community of over 60K unique users and 500K+ total NFTs. Although decentralized applications (dApps) can help to limit the influence of specific parties or people, the HEN incident is an interesting case study that shows how restricting access to the “official” front end (i.e., how users interact with the underlying smart contracts) of a dApp can cause immediate disruption. For example, the daily number of NFTs (called OBJKT’s on HEN) minted on the platform fell from ~3,300 on November 11th to ~1,300 on November 12th.

Similarly, the number of HEN NFTs being transferred (swapped) on the Tezos blockchain also fell following the shut down, from ~8,600 on 11/11 to ~3,500 on 11/12.

The sudden shutdown has seemingly impacted macro-level statistics on Tezos, as NFTs have become a significant driver of traffic on the network. The daily number of active addresses (on the sending side of a ledger change, to remove the noise of addresses receiving staking rewards roughly every 3 days) increased closely with HEN activity in August and September. But in the days since the HEN website shut down, active addresses on the network have decreased.

Source: Coin Metrics Formula Builder

Although there has clearly been a short-term impact, the underlying smart contracts were untouched and live on on the Tezos blockchain. In fact, the number of daily OBJKTs being minted and swapped have started to bounce back as collectors and artists turn to alternative tools and new front ends. Despite the uncertainty and interruption, the HEN community appears to be stepping up, showing the resiliency of dApps with strong communities and the merits of web3.

To follow the data used in this piece and explore our other on-chain metrics check out our free charting tool, formula builder, correlation tool, and mobile apps.

Network Data Insights

Summary Metrics

Source: Coin Metrics Network Data Pro

Although market caps ticked up over the last week, other major on-chain metrics were mostly flat. Bitcoin transactions grew by 2.9% week-over-week while Ethereum transactions dropped by 0.6%. Stablecoin activity also dropped off after a recent surge. Tether (USDT) active addresses declined by 2.1% on the week, while USDC active addresses fell by 8.9%.

Network Highlights

Check out our new weekly summary video which breaks down some key metrics for Bitcoin, Ethereum, and stablecoins.

Coin Metrics Updates

This week’s updates from the Coin Metrics team:

Python users! Check out the Coin Metrics Python API client to query CM market & network data for both community & pro users.

Check out our market-data focused newsletter State of the Market, featuring weekly updates on market conditions.

As always, if you have any feedback or requests please let us know here.

Subscribe and Past Issues

Coin Metrics’ State of the Network, is an unbiased, weekly view of the crypto market informed by our own network (on-chain) and market data.

If you'd like to get State of the Network in your inbox, please subscribe here. You can see previous issues of State of the Network here.

Visit the Coin Metrics Blog for more in depth research and analysis.

© 2021 Coin Metrics Inc. All rights reserved. Redistribution is not permitted without consent. This newsletter does not constitute investment advice and is for informational purposes only and you should not make an investment decision on the basis of this information. The newsletter is provided “as is’ and Coin Metrics will not be liable for any loss or damage resulting from information obtained from the newsletter.