Coin Metrics' State of the Network: Issue 134 - 2021 Year in Review

Tuesday, December 21st, 2021

The State Of The Network 2021 Year In Review

By Nate Maddrey and Kyle Waters

Get the best data-driven crypto insights and analysis every week:

In this special edition of State of the Network we look back at crypto’s biggest storylines of 2021. To explore the data used in this piece check out our free charting tool, formula builder, correlation tool, and mobile apps.

Source: Coin Metrics Reference Rates (YTD through 12/21 midnight UTC)

Q1: Bitcoin Boom

After a tumultuous 2020 bitcoin (BTC) entered 2021 on a high. Seven out of the first eight days of the year marked new all-time highs for BTC, with price topping $40K for the first time on January 8th largely thanks to a new inflow of institutional investors. After macro conditions changed in 2020 in response to the onset of the COVID-19 pandemic, large institutions started to publicly enter the crypto market en masse, which continued into the start of 2021.

Then in early February a surprise announcement sent the market to new heights: Tesla entered the picture with a $1.5B purchase of BTC. By February 21st BTC had surged to over $57.5K, already up 96% from January 1st. The number of BTC wallets holding a balance greater than 0 grew by about 5.8M over the course of 2021. But the largest growth occurred in Q1 following Tesla’s announcement.

Source: Coin Metrics Network Data Charts

Historically, after BTC surges investors begin to rotate into small-cap cryptos. This year was no different with an unprecedented surge of layer-1 assets and small-cap tokens. Dogecoin (DOGE) helped usher in a new wave of memecoins in Q1, which would become a theme throughout the year. DOGE suddenly spiked from under $.0075 to about $.05 between January 27th and 29th after a new wave of buyers rushed in.

Q1 also marked the first major surge for non-fungible tokens (NFTs). After quietly building up for years NFTs began to explode in February and March 2021. The initial NFT rally was accentuated by Beeple’s $69M NFT sale at Christie’s on March 11th, which helped NFTs gain mainstream attention, but also marked the top of the Q1 NFT boom.

Q2: Miner Migration

With the long anticipated Coinbase IPO finally happening on April 14th, the traditional financial sector’s interest in bitcoin and crypto was approaching a new peak. Looking back, April 13th marked BTC’s highest daily close of the first half of the year, topping out at $63.45K.

In addition to BTC and DOGE, most other cryptos also surged to new highs during Q2. Benefitting from the new users brought on by the growing popularity of NFTs, ETH shot to a new all-time high of over $4.1K on May 11th. Solana (SOL) also started its surge and topped $50 for the first time in mid-May. Decentralized finance (DeFi) tokens like Uniswap (UNI), Compound (COMP), and AAVE also surged to new highs in April and May, dwarfing 2020’s DeFi summer. In hindsight, May marked the top for most major DeFi assets, which underperformed during the second half of the year.

But soon after the May surge a series of negative events turned the market on its head. After initially extolling BTC, Elon Musk and Tesla changed their tune just three months after entering the market. On May 12th, Musk announced that Tesla was suspending purchases using BTC due to concerns over Bitcoin’s energy consumption.

Almost simultaneously, an even more serious situation started to develop: the Chinese government announced a regulatory crackdown of Bitcoin mining and trading. Although China has “banned” Bitcoin several times in the past, this time was different: Chinese Bitcoin miners started to shut down and rapidly leave the country in anticipation of regulatory action. The amount of BTC transferred by miners hit a yearly high as some miners moved to sell their holdings and move out of the country.

Source: Coin Metrics Network Data Charts

Following the news, the market began to tumble. The back-to-back shockwaves led to a major liquidation cascade as futures contracts were forcibly sold, leading to a sudden dip to about $30K.

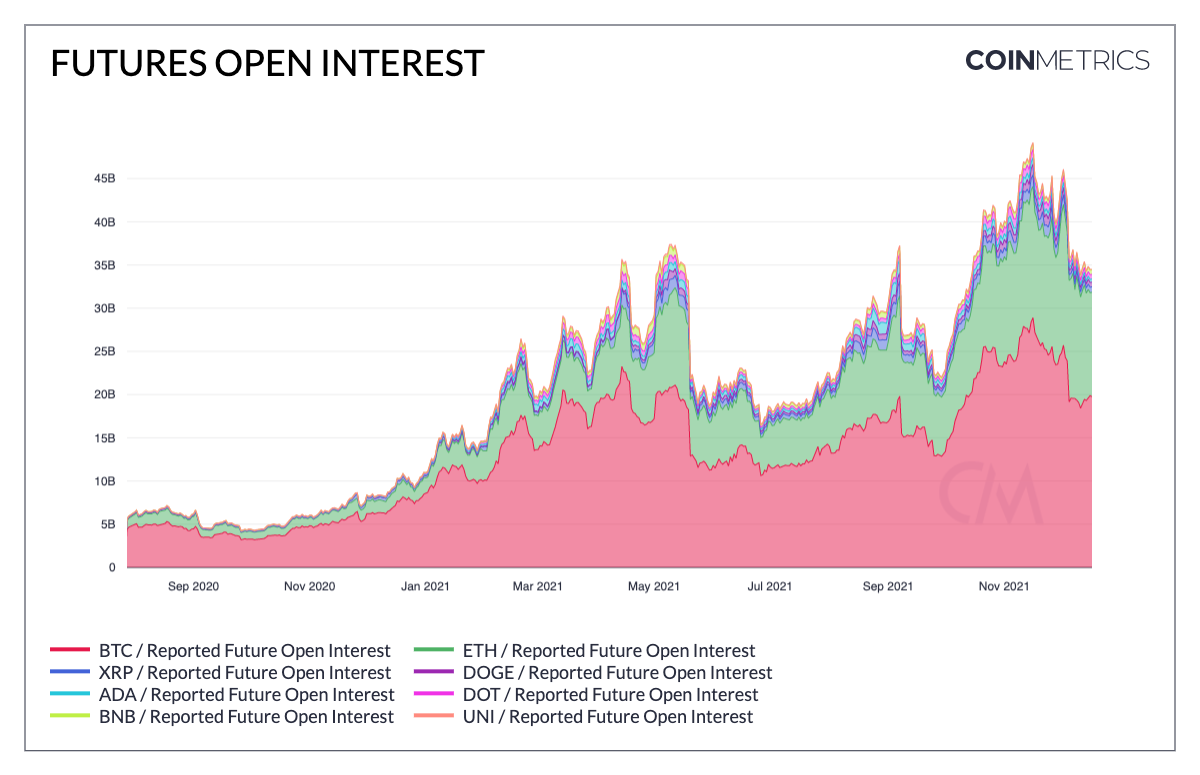

Although the series of bad news was a sure catalyst, the market was already on shaky ground - by May 11th many crypto assets had record high levels of open interest, which indicates there was likely a high amount of leverage in the futures market (since contracts are often opened using leverage). High levels of leverage leaves the market vulnerable during unexpected, sudden volatility.

High open interest and the accompanying leverage would be a theme throughout the year with open interest reaching even higher levels later on in 2021. However, the May crash also helped lead to some industry-wide change, as Binance and FTX both reduced their leverage limit to 20x in July.

Source: Coin Metrics Network Data Charts

In the wake of the crash, stablecoins experienced major growth as investors rushed to safety. Although Tether (USDT) is still the largest stablecoin by market cap, USDC had a particularly strong year - USDC supply on Ethereum increased by about 50% between May 18th and June 18th alone, and has outpaced USDT growth since the start of 2021.

Although it was a tumultuous quarter, Q2 closed with some positive momentum: BTC officially became legal tender in El Salvador, marking the first nation to recognize BTC as a satisfactory form of payment for any form of monetary debt. El Salvador’s adoption helped spur Lightning Network activity - the number of public Lightning Channels has increased from 49K to 86K since June 1st.

Q3: JPEG Summer

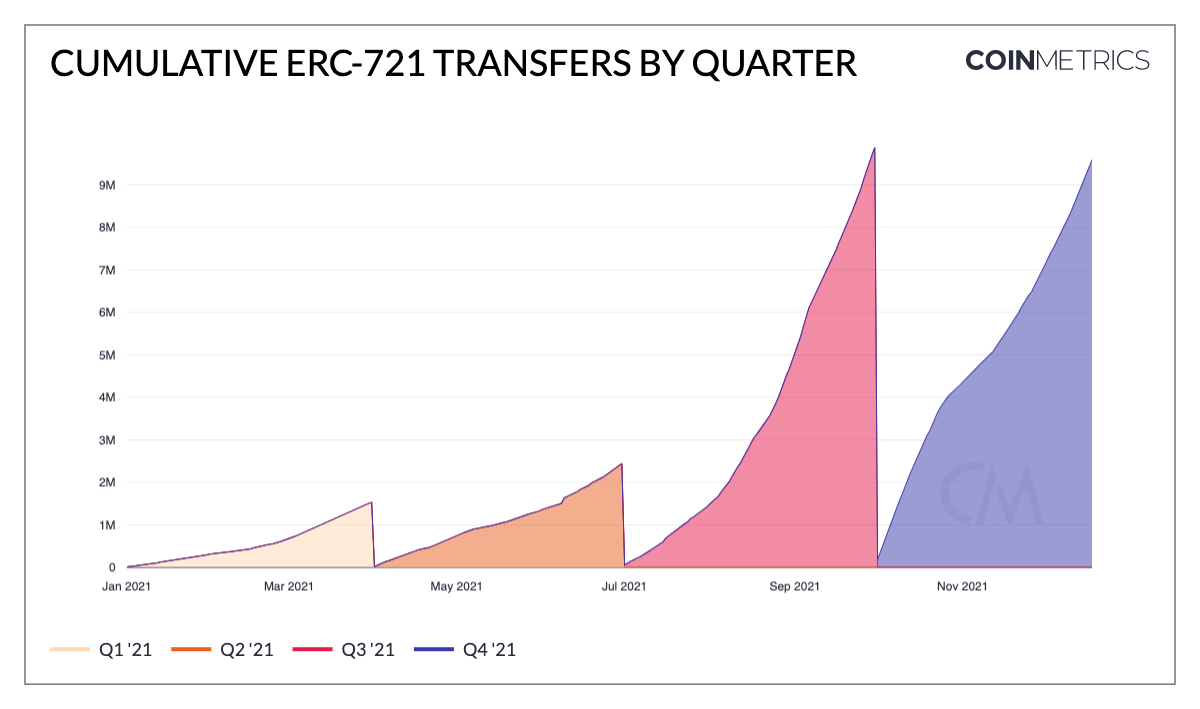

After an initial boom in Q1, NFTs took a back seat to the rest of the crypto market during Q2. But then, in the wake of the May crypto crash, NFTs suddenly exploded.

It took until only August 12th for total transfers of ERC-721 tokens (the standard for NFTs on Ethereum) in Q3 to surpass Q2’s total. There were over 2.4M transfers recorded in the first ~6 weeks of the quarter alone, and 9.9M in all of Q3 – a 305% increase QoQ.

Source: Coin Metrics Network Data Charts

In a sign of institutional interest in NFTs, payments powerhouse Visa announced in late August that they had purchased a CryptoPunk. CryptoPunks, which first launched in 2017, were among the most highly sought after NFTs in 2021 and recently capped off the year as the highest-weighted constituent in crypto asset manager Bitwise’s new Blue-Chip NFT Fund. The demand for Punks in 2021 left a visible imprint on-chain with Punks changing hands at an unprecedented rate.

The chart below shows the percentage of CryptoPunks supply last active by time period (often referred to as “HODL Waves”). The brown/red/yellow bands towards the bottom of the chart represent the % of supply that was active (i.e. transferred) more recently in the last 3 months while the bands at the top (blues & purples) show the portion of supply held for longer. Punks moved around at a record pace in 2021, with 75% or 7.5K of the 10K total Punks moving on-chain at least once. The number of unique ETH addresses owning a Punk more than tripled in 2021 from ~1K to 3.3K.

For more information on how we create CryptoPunks HODL Waves and other NFT analytics, check out our special 2021 report on The Rise of NFTs .

But by the end of September, the NFT run had started to deflate. A combination of a flood of new supply (both from existing projects and a deluge of new projects popping up overnight), high gas fees, and rising ETH price (NFTs are often priced in ETH) caused NFTs to cool off by the start of Q4. Daily NFT sales on OpenSea peaked in the first week of October at over 85K sales but quickly fell back to early summer levels by November.

Simultaneously, Ethereum underwent one of its most significant changes since genesis in EIP-1559. Launched on August 5th after much anticipation, EIP-1559 brought a major update to Ethereum’s fee mechanism. A key feature of EIP-1559 was the introduction of a protocol-determined base fee that fluctuates with demand for block space. To avoid creating adverse incentives for miners to game block sizes, this base fee is “burned,” permanently removing that ETH from circulating supply. Partially thanks to NFTs and increased activity in general, over 1.2M ETH has now been burned since the introduction of EIP-1559. Ethereum’s monetary policy has changed dramatically, with ETH’s net annual inflation rate falling as a result of the new fee burn.

Source: Coin Metrics Network Data Charts

But with activity and fees rising, further scrutiny was placed on Ethereum and its scalability woes. High fees on Ethereum inspired users to adopt and migrate to a new wave of alternative layer one (L1) smart contract platforms. Solana (SOL), Avalanche (AVAX), and others all hit new all-time highs while fostering competing ecosystems of NFTs and DeFi. But the race to scale heated up with Ethereum layer 2 (L2) solutions such as Arbitrum gaining increased adoption. NFTs served as a general crypto gateway and with many new participants entering the ecosystem, big tech and other investors started taking a fresh look at the space going into Q4.

Q4: Into the Metaverse

On October 15th, after a long wait, a bitcoin-focused ETF finally launched in the U.S. However, the ProShares Bitcoin Strategy ETF (BITO) was a futures ETF, not a spot ETF product. Despite being a more indirect exposure to spot BTC, BITO saw record inflows and volume traded on its first day making it one of the largest ETF launches ever.

By October 19th BTC price topped $64K, surpassing Q2’s top and setting a new all-time high. Q4 also ushered in Bitcoin’s biggest upgrade in four years: Taproot. Taproot introduced new scripting possibilities and laid the foundation for new smart contract functionality, while improving Bitcoin’s security and privacy. So far, about 1.6K BTC has been stored in Taproot P2TR outputs.

ETH would soon follow BTC’s lead, hitting a new all-time high of $4.8K on November 8th. At the same time, the narrative around Ethereum and other smart contracts started to shift. Ideas surrounding Web3, a vision of a decentralized web, started to gain traction in Q4. Decentralized Autonomous Organizations (DAOs) gained momentum with the most celebrated example, ConstitutionDAO, raising $45M in under a week.

The Web2 tech macro landscape started to reflect changing narratives as well. Square announced that it would be rebranding to “Block,” and Facebook announced on October 28th that its name would change to “Meta,” accelerating interest in the metaverse. ERC-20 token prices for virtual land projects like Decentraland and Sandbox took off relative to ETH after this announcement.

Source: Coin Metrics Reference Rates

Back in the real world, macro conditions were once again shifting with inflation hitting a 39-year high. Towards the end of the quarter, the Fed announced the potential for a more aggressive pace of interest rate increases in 2022. The market-implied probability of a rate hike by March 2022 now stands at 47.4%, up from 25.2% at the beginning of December.

With a huge year behind us and shifting macro conditions going into 2022 the crypto markets are entering uncharted territory. Carried by the continued momentum of L2s, NFTs, Web3, Taproot, and the potential launch of Ethereum 2.0, 2022 is lining up to be another transformational year for crypto.

2021 Network Highlights

Bitcoin had a record year. Using Coin Metrics’ adjusted transfer value metric, Bitcoin settled a total of $4.5T in 2021. The following table presents on-chain data highlights in 2021 for Bitcoin, Ethereum, Tether, and USDC.

Source: Coin Metrics Network Data Pro

Also be sure to check out our end-of-year data animations for BTC, ETH, and Stablecoins.

Subscribe and Past Issues

Coin Metrics’ State of the Network, is an unbiased, weekly view of the crypto market informed by our own network (on-chain) and market data.

If you'd like to get State of the Network in your inbox, please subscribe here. You can see previous issues of State of the Network here.

Check out the Coin Metrics Blog for more in depth research and analysis.

© 2021 Coin Metrics Inc. All rights reserved. Redistribution is not permitted without consent. This newsletter does not constitute investment advice and is for informational purposes only and you should not make an investment decision on the basis of this information. The newsletter is provided “as is’ and Coin Metrics will not be liable for any loss or damage resulting from information obtained from the newsletter.