Coin Metrics' State of the Network: Issue 136

Tuesday, January 4th, 2022

Get the best data-driven crypto insights and analysis every week:

Crypto’s Biggest Storylines Going Into 2022

By Kyle Waters and Nate Maddrey

After a transformative 2021 marked by new all-time highs for most of the major cryptoassets and key on-chain metrics, expectations are high for crypto in 2022. In this issue of State of the Network, we analyze some of the most important trends and stories to watch in the new year.

The Global Macroeconomic Landscape & Bitcoin’s Role as an Inflation Hedge

Throughout its history, the key narratives surrounding Bitcoin have undergone many changes with an ever evolving world. While the reasons to own bitcoin (BTC) still vary, the perception of BTC as an attractive hedge to inflation has accelerated in the last couple of years following the unprecedented fiscal and monetary response to the COVID-19 pandemic across the world.

Bitcoin’s property as an untamperable and non-inflatable store of value helped drive institutional interest in 2020 & 2021. In May 2020, hedge fund manager Paul Tudor Jones declared that we are witnessing the “Great Monetary Inflation” with the “expansion of every form of money” and made a case for owning bitcoin – what he called the “quintessence of scarcity premium” that is “literally the only large tradable asset in the world with a known fixed maximum supply.” In October 2021, Jones announced that his portfolio contained crypto holdings in the “single digits.”

Bitcoin was designed as a deflationary currency with a fixed total supply that is programmatically set to max out at 21M BTC. The BTC issuance schedule follows a predetermined set of protocol rules known to all, with the amount of new BTC issued via block rewards cut in half (“halving”) every 210K blocks or roughly every 4 years. More than 90% of all BTC that will ever exist has now been issued and in 2021 BTC supply increased by just 1.8%. The next halving will occur in May 2024.

Source: Coin Metrics’ Network Data Charts

In another now well-documented case study, in August 2020 Microstrategy adopted bitcoin as its primary treasury reserve asset citing that the “decision to invest in bitcoin at this time was driven in part by a confluence of macro factors” and would “provide not only a reasonable hedge against inflation, but also the prospect of earning a higher return than other investments.”

With inflation in the US recently hitting a 39-year high of 6.8% YoY in November and the Federal Reserve dropping the word “transitory” to describe this latest bout of inflation, these decisions now seem especially prescient. Bitcoin seems poised in 2022 to continue benefiting from its role as an inflation hedge. But there is still some structural and macroeconomic uncertainty.

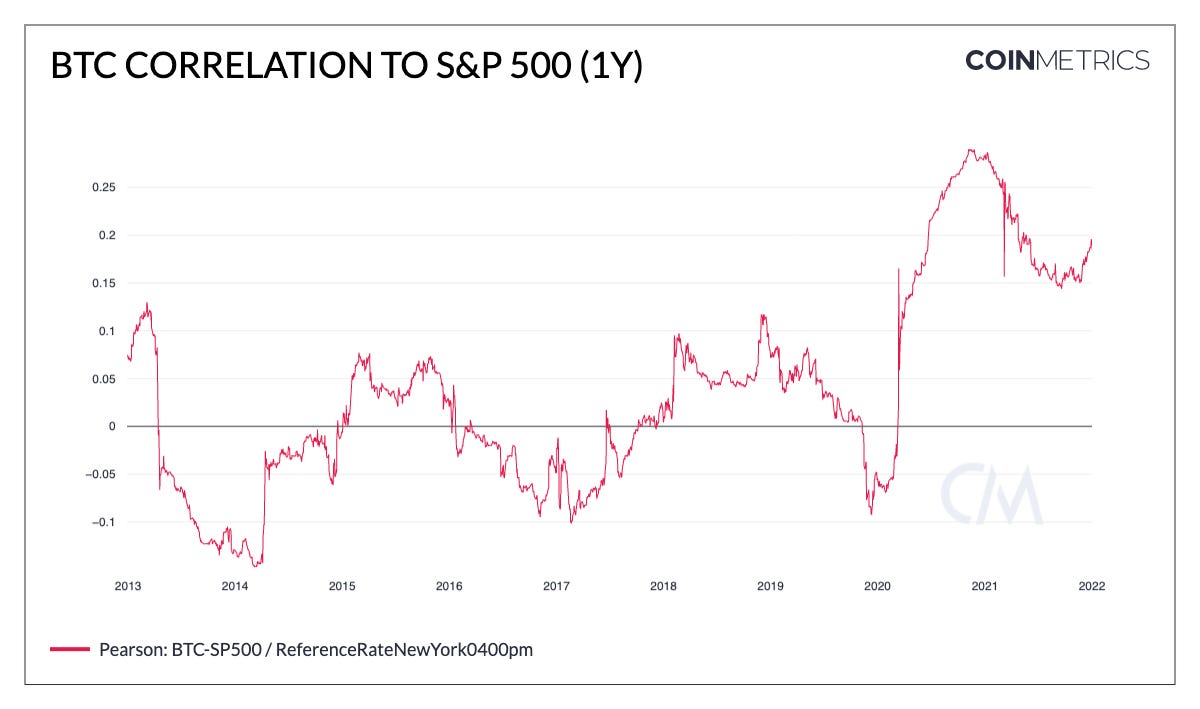

First, bitcoin’s correlation to US equities has been persistently positive since the marketwide sell-off at the onset of the COVID-19 pandemic. The current correlation of ~0.2 using a one-year window of BTC and S&P 500 daily returns is relatively low, but historically BTC’s returns have been more detached from the broader market which is generally an attractive characteristic for portfolio construction. From a structural standpoint, if BTC is moving more in line with other volatile assets like stocks this might dampen BTC’s narrative as a hedge.

Source: Coin Metrics’ Correlation Tool

Another question mark is the action(s) central bankers will take in 2022 to fight rising inflation. In a shift in tone, the Fed’s December policy statement announced that “in light of inflation developments” it would reduce the pace of its monthly asset-purchasing program. Projections from the Fed also indicated that policymakers envisioned three interest-rate hikes in 2022. According to data from the Federal Reserve Bank of Atlanta, the market-implied probability of a 0.25% rate hike by March 14th of this year now stands at 62%, rising from just 18% at the end of October.

But even as US policymakers change their stance, the macro outlook elsewhere remains uncertain. Inflation in the euro zone is also running hot at 4.9%, and far more precarious situations exist in places like Turkey where the country’s lira has collapsed against the dollar amid an inflationary spiral. With inflation running over 20%, Turks have already turned to alternative stores of value, which might include bitcoin and other cryptoassets or dollar-backed stablecoins.

If we are truly in the era of the Great Monetary Inflation, more institutions and individuals in 2022 across the world might be drawn to bitcoin’s assured scarcity.

“The Merge”: Will Ethereum Take its Next Step in the ETH 2.0 Roadmap?

In August 2021, Ethereum core developers implemented EIP-1559 which changed Ethereum’s fee market mechanism and was one of the most significant upgrades to the protocol since its 2015 genesis. With roughly five months worth of data, EIP-1559 now seems to have been largely successful in lowering fee market variability and reducing overpayment.

Entering 2022, another significant change is expected to be on the horizon for Ethereum: “The Merge,” the upcoming event of swapping out Ethereum’s current proof of work (PoW) consensus algorithm for a proof of stake (PoS) consensus mechanism.

Mechanically, The Merge and move to PoS should have minimal impact on applications currently running on Ethereum and nothing will happen to ETH that is held by current users. In fact, the Ethereum EVM will not be deprecated and will remain as the execution layer post-merge.

After several iterations of the ETH 2.0 vision, the first set of changes that comprise ETH 2.0 launched in November 2020. Dubbed “Phase 0”, the creation of the beacon chain introduced the PoS consensus mechanism for ETH 2.0 and the ability to register as a validator by depositing a minimum of 32 ETH to the official deposit contract. Over 8.8M ETH has now been deposited to the ETH 2.0 staking contract, with around 277K total validators.

Staking introduces a way for holders to earn yield on their ETH, and also serves as a supply sink as large amounts of ETH is locked into the deposit contract, effectively lowering free float supply. Staking rewards are dependent on the amount of ETH staked, and gradually decrease as more ETH gets deposited.

Outside of solo staking, there are a few different methods to stake ETH. Many centralized exchanges offer custodial staking services and stake ETH on their customers’ behalf. Other more decentralized solutions exist such as Lido and Rocket Pool. The following chart shows the total ETH staked in the Ethereum 2.0 staking contract broken out by depositor, tagging the addresses for some of the largest staking services (hobbyists are broadly defined as addresses that have only contributed the minimum 32 ETH, and no more).

Current estimates pin the potential timing of The Merge in Q2 or Q3 of this year, however there is still uncertainty about the exact launch date. The move to PoS will have several implications for Ethereum, its cryptoeconomics, miner extractable value (MEV), staking derivatives, and more making it one of the most important areas of crypto research in 2022.

The Rise of L2s

In 2021, as Ethereum transaction fees hit new record highs, some users and investors turned to competing smart contract platforms that could offer lower fees. Solana (SOL), Avalanche (AVAX), Algorand (ALGO) and others experienced record growth in 2021 in the battle to be the next big smart contract layer-1 (L1).

But going into 2022 we’re on the cusp of a new scalability war: the battle of the layer-2s (L2s). L2s are built on top of an existing blockchain to improve transaction scalability while maintaining the underlying blockchain’s security. For example, some L2s use rollups to execute transactions off-chain while eventually committing transaction data back to Ethereum’s layer-1. This helps increase transaction speed and allows for lower fees while maintaining Ethereum’s decentralization and security.

Several major Ethereum L2s launched late in 2021, including Arbitrum, Optimism, Starknet, and zkSync. DeFi protocols like Maker, Uniswap, SushiSwap, and AAVE all announced L2 integrations. Additionally, applications that help users move funds and trade across L2s started to launch in 2021. Hop Exchange, for example, provides an interface for bridging between Ethereum, Arbitrum, Optimism, xDai, and Polygon. Slingshot, also launched in 2021, is an L2 trading platform that aggregates the largest decentralized exchanges (DEXs) across Arbitrum, Polygon, and others. The successful adoption of L2s would open up new use-cases for on-chain games, NFTs, and DeFi applications that could offer low fees while still benefiting from the rest of the Ethereum ecosystem.

Bitcoin also started to see the rise of L2s in 2021. Lightning Network, a payment channel based L2 solution that enables fast, low-fee transactions, saw its largest growth ever throughout 2021. Going into 2022 there’s over 3.3K BTC held across 86.41K public Lightning channels, up from 1.07K and 38.05K (respectively) since January 1st, 2021.

L2s still face a lot of challenges, including sometimes complicated UX, and high costs of moving funds to and from an L2. But successful L2 scaling could unleash a new Cambrian explosion of usage and development going into 2022.

The Impact of Crypto Regulation

Last May, the Chinese government began a regulatory crackdown on Bitcoin mining and crypto-related activities in the country. Although Bitcoin had been “banned” many times before in China, last year was different with miners and exchanges rapidly shutting down and leaving. These actions created many shockwaves across the global crypto industry and it is still unclear what all of the ramifications will be in 2022 and beyond.

One area that is currently still in flux is crypto exchanges. Huobi, one of the largest exchanges in the world by trading volume, is currently in the process of winding down operations in mainland China after the country’s regulators intensified their intervention on crypto activities in September of last year. BTC and ETH held on Houbi have plummeted as the exchange has been forced to shut down existing user accounts and mining activity shifts to the West.

Source: Coin Metrics’ Network Data Charts

The shifting mining activity out of China has helped create the conditions for a vibrant new ecosystem of operations in the United States and the West more generally. With Bitcoin miners receiving total revenue to the tune of $16.8B in 2021, new operations are in the works and new hash power in the US is set to come online in 2022.

But even as Bitcoin mining becomes an increasingly US industry, regulators in the US are further scrutinizing crypto activity. As their total supply nears $150B, stablecoins have been an important topic of conversation in particular, with the President’s Working Group on Financial Markets releasing a report on the subject in November of last year. SEC Chairman Gary Gensler has publicly called for new regulations for crypto exchanges and the potential for additional oversight.

Regulation is set to be a topic of intense discussion in 2022 with the potential to bring significant changes (and likely welcomed clarity) for the crypto industry.

To follow the data used in this piece and explore our other on-chain metrics check out our free charting tool, formula builder, correlation tool, and mobile apps.

Network Data Insights

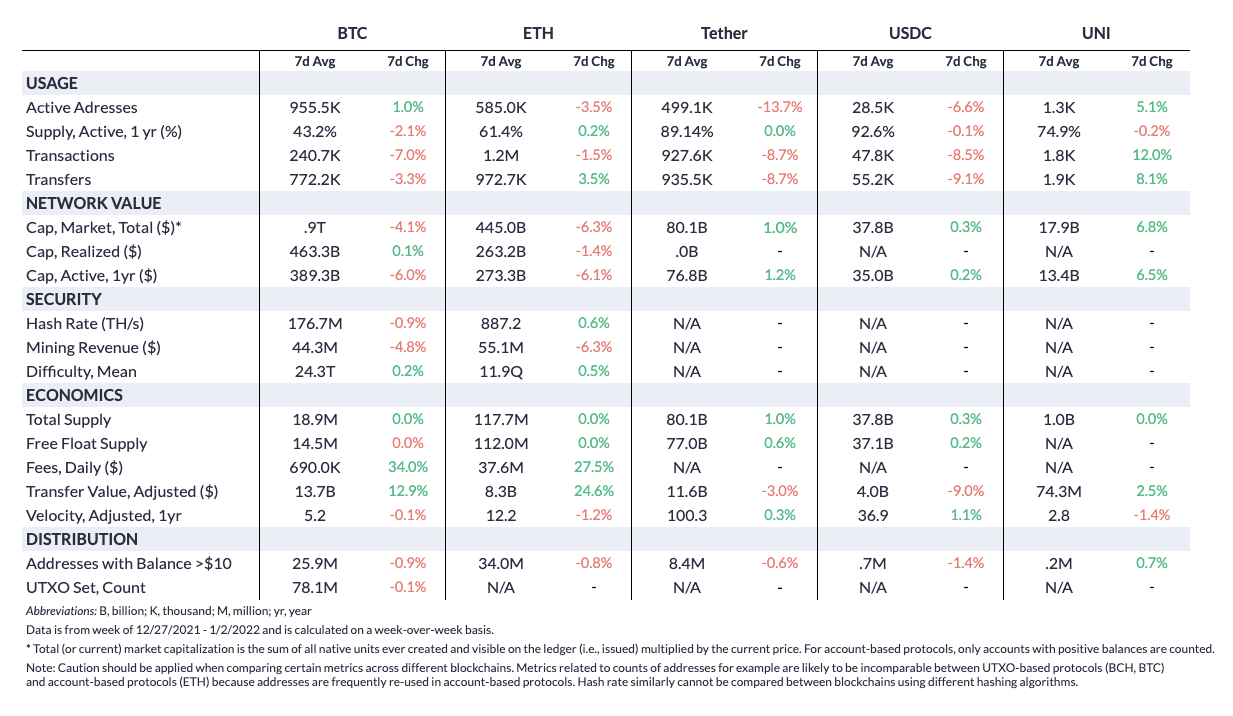

Summary Metrics

Source: Coin Metrics Network Data Pro

Bitcoin (BTC) and Ethereum (ETH) on-chain activity cooled off going into the end of 2021 as BTC market cap fell back under $1T. BTC averaged 955.5K daily active addresses over the last week while ETH averaged 585K. Hash rate growth for both chains was also relatively flat, with Bitcoin declining by 0.9% week-over-week and Ethereum growing by 0.6%. Additionally, stablecoin usage dipped over the last week of the year, with Tether daily active addresses (across Ethereum, Tron, and Omni) dropping to below 500K on average.

Network Highlights

Check out our weekly network highlights summary video:

Coin Metrics Updates

This week’s updates from the Coin Metrics team:

Check out our market-data focused newsletter State of the Market, featuring weekly updates on market conditions.

Also check out the Coin Metrics mobile app. View real-time cryptoasset pricing and relevant on-chain data in a single app! Download for free here: https://coinmetrics.io/mobile-app/

As always, if you have any feedback or requests please let us know here.

Subscribe and Past Issues

Coin Metrics’ State of the Network, is an unbiased, weekly view of the crypto market informed by our own network (on-chain) and market data.

If you'd like to get State of the Network in your inbox, please subscribe here. You can see previous issues of State of the Network here.

Check out the Coin Metrics Blog for more in depth research and analysis.

© 2021 Coin Metrics Inc. All rights reserved. Redistribution is not permitted without consent. This newsletter does not constitute investment advice and is for informational purposes only and you should not make an investment decision on the basis of this information. The newsletter is provided “as is’ and Coin Metrics will not be liable for any loss or damage resulting from information obtained from the newsletter.