Coin Metrics' State of the Network: Issue 20

Tuesday, October 8th, 2019

Weekly Feature

Tezos Market Cap Bounced Back in 2019, But Still Has Little Usage

After a controversial start, Tezos (XTZ) has bounced back in 2019. Since the start of 2019, XTZ’s market cap has grown almost in lock step by BTC’s. As of October 6th, XTZ’s market cap has grown by 119%, while BTC’s has grown by 112%.

XTZ’s realized market capitalization grew over the course of 2019. Realized capitalization is a metric created by Coin Metrics that is calculated by valuing each unit of supply at the price it last moved. This is in contrast to traditional market cap which values each coin uniformly at the current market price. Realized cap can be thought of as a measure of the average cost basis of asset holders (cost basis is basically the total amount originally invested). Check out State of the Network Issue 14 for a more detailed explanation of realized cap.

XTZ’s realized cap has grown by over 10% since the beginning of 2019, while BTC’s grew by over 28%. ETH, ADA, DCR, and ZEC’s realized caps have all declined over the course of 2019.

Even though XTZ’s market cap has been growing, its network activity has not been growing at a similar rate. The below chart shows XTZ’s daily active addresses. We define “active addresses” as the unique number of addresses that either sent or received a ledger change over the course of a day. Users may own multiple addresses, so active addresses serves as the upper bound for potential amount of daily unique users on a network.

Over the last 30 days, XTZ has had an average of 4,803 active addresses, compared to 286,467 and 709,569 daily active addresses for ETH and BTC, respectively.

Additionally, the following chart shows XTZ’s daily transaction count and daily transfer count. We define a “transfer” as any transaction that moves some units of XTZ between two addresses. “Transactions” include all types of ledger amending actions, including contract calls and other non-monetary operations.

XTZ’s transaction count is significantly higher than its transfer count, which signifies that a majority of Tezos operations are non-monetary. This ratio differs from blockchain to blockchain; over the last 30 days, ETH has about 2.3x as many transactions as transfers, while BTC has had over 2.15x transfers as transactions.

Digging deeper, the below chart shows XTZ’s transaction count broken down by operation type. A majority of XTZ transactions are endorsements. Endorsements are part of the Tezos baking process, and occur every time a block is baked. Tezos also has a significant amount of account activations, delegations, originations, and reveals, which are all part of the Tezos baking and account creation processes.

Filtering out endorsements, account activations, delegations, originations, and reveals, we are left with all other transactions, which can be seen as the “transaction” line in the below chart (which uses a log scale).

Over 95% of the remaining transactions are transfers (i.e. 95% of the remaining transactions that are not endorsements, account activations, delegations, originations, or reveals are transfers). This means that there are only a small amount of other types of non-monetary XTZ transactions, such as non-monetary contract calls.

In fact, XTZ has a small number of contracts overall. As of October 6th, XTZ only has 108 contracts that contain code. This compares to over 11,000,000 contracts with code on Ethereum.

Although Tezos’ market cap has been showing signs of growth, it still has a long way to go in terms of gaining real adoption.

Network Data Insights

Summary Metrics

BTC’s market cap and realized cap continued to slide over the past week, dropping by 3.1% and 0.4%, respectively. ETH’s market cap, on the other hand, grew a little over the last week, with a 1% growth in market cap and 0.7% growth in realized cap. ETH’s active addresses also surged upwards, growing by over 15.5%.

Adjusted transfer value for both BTC and ETH also dropped significantly over the past week, both down by over 28%. LTC and BCH’s adjusted transfer value also had a bad week, each dropping by over 47%. XRP, however, escaped the onslaught. XRP’s adjusted transfer value grew by 22.5% week over week.

Network Highlights

ETH continues to challenge BTC for the daily transaction fees throne. ETH daily fees briefly passed BTC daily fees on both September 28th and 29th, by a margin of about $20,000 on both occasions. However BTC has once again taken the lead since then. On October 6th, BTC had over $128,000 daily fees, compared to a little over $66,000 for ETH.

BTC’s total fees (i.e. all-time cumulative fees) are approaching $1,000,000,000. As of October 6th, BTC has $990,237,685 of total fees. BTC’s total fees should pass the billion dollar milestone on approximately October 14th. Coincidentally, BTC all-time miner revenue (which includes fees and block rewards) should reach $15 billion around approximately the same time, give or take a day or two.

Market Data Insights

Tether on Ethereum Almost Exceeding Tether on Omni

The long-term trend of Tether supply shifting from the Omni protocol to a ERC-20 token on the Ethereum blockchain continues. Coin Metrics has previously written about the current state of stablecoins and Tether supply.

Although Tether has not publicly disclosed why they are swapping supply issued on Omni to Ethereum, market forces indicate that this trend should continue. Possible explanations include a concerted effort to diversify away from a single, largely unmaintained protocol in Omni and taking advantage of the robust wallet, tools, and infrastructure supporting ERC-20 tokens. As Tether is primarily used for active traders engaged in arbitrage, transacting Tether through Ethereum brings many advantages, including faster time to first confirmation, faster exchange withdrawal and deposit times, and lower fees. On the margin, increased issuance of Tether on Ethereum should be supportive of higher transaction counts and fees, while reducing these figures on Bitcoin.

The current Tether supply is 4.1 billion units, consisting of 2.15 billion on Omni and 1.96 billion on Ethereum. There are also minuscule amounts of Tether issued on other blockchains, including 0.14 billion on Tron and 0.005 billion on EOS. The latest significant change in supply occurred on September 16 when the Tether Treasury burned 400 million units on Omni and issued the same amount on Ethereum with a short lag. Over the past several days, small amounts of Tether have been printed on Ethereum.

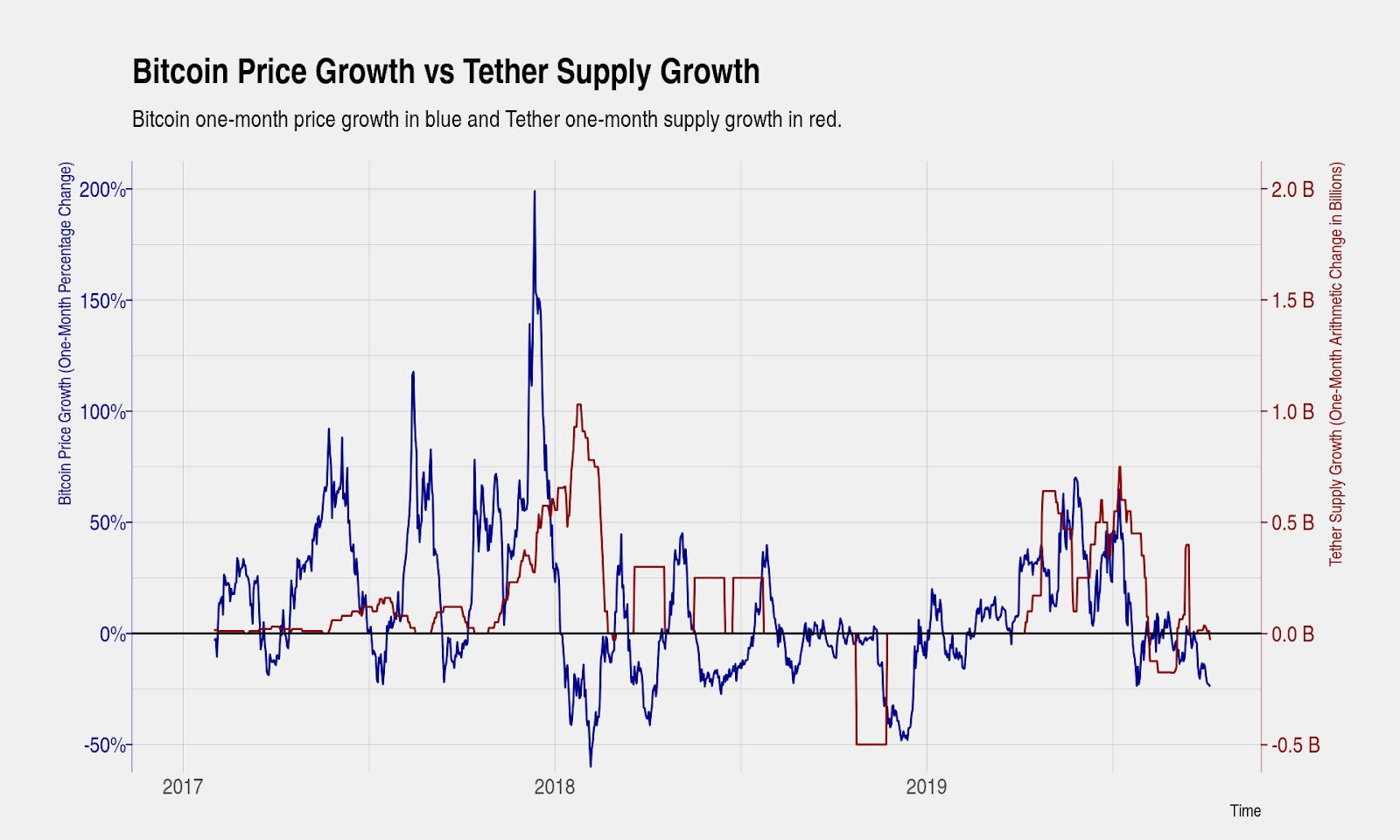

Declines in Tether Supply Provide More Observations to Study Relationship with Bitcoin Price

Although the specific mechanism behind why additional Tether is printed is unknown, several explanations have been put forth. One set of explanations, advocated by representatives of Tether, is that Tether will occasionally print Tether to fulfill future purchase obligations by traders. Tether is printed in large batches purely as a means of convenience. Another set of explanations are conspiratorial in nature and suggest that Tether and its affiliated entities may engage in price manipulation. The lack of transparency drives these explanations.

Regardless of which explanation is closest to the truth, both sets of explanations could suggest a relationship between Tether printing and future price movements. There is also a second order effect in that this narrative is widely known and followed, to the extent that this belief could drive trader behavior and make this relationship self-fulfilling.

Recent changes in Tether supply provide more observations to study this relationship. In August, the Tether Treasury burned 300 million Tether on Omni, resulting in only the second time in history that Tether supply has decreased. Below we plot the one-month change in Bitcoin’s price in blue with the one-month change Tether supply in red. Recent price movements have revealed that Bitcoin price declined following the decline in Tether supply (with a short lag) as it did during a similar situation in late 2018.

The relationship between Tether supply and Bitcoin price deserves continued study. Promising areas of research include analysis of the exact timing of transactions between the Tether Treasury and exchanges, controlling for Tether supply that remains in the Tether Treasury or is otherwise quarantined, and exploring the relationship at different lags. Despite the increased regulatory scrutiny and the mounting lawsuits against Tether, it still remains a critically important element in crypto markets and its systemic importance continues to grow. The market share of Tether trading volume has recently reached nearly 75 percent on Binance and shows long-term growth.

CM Bletchley Indexes (CMBI) Insights

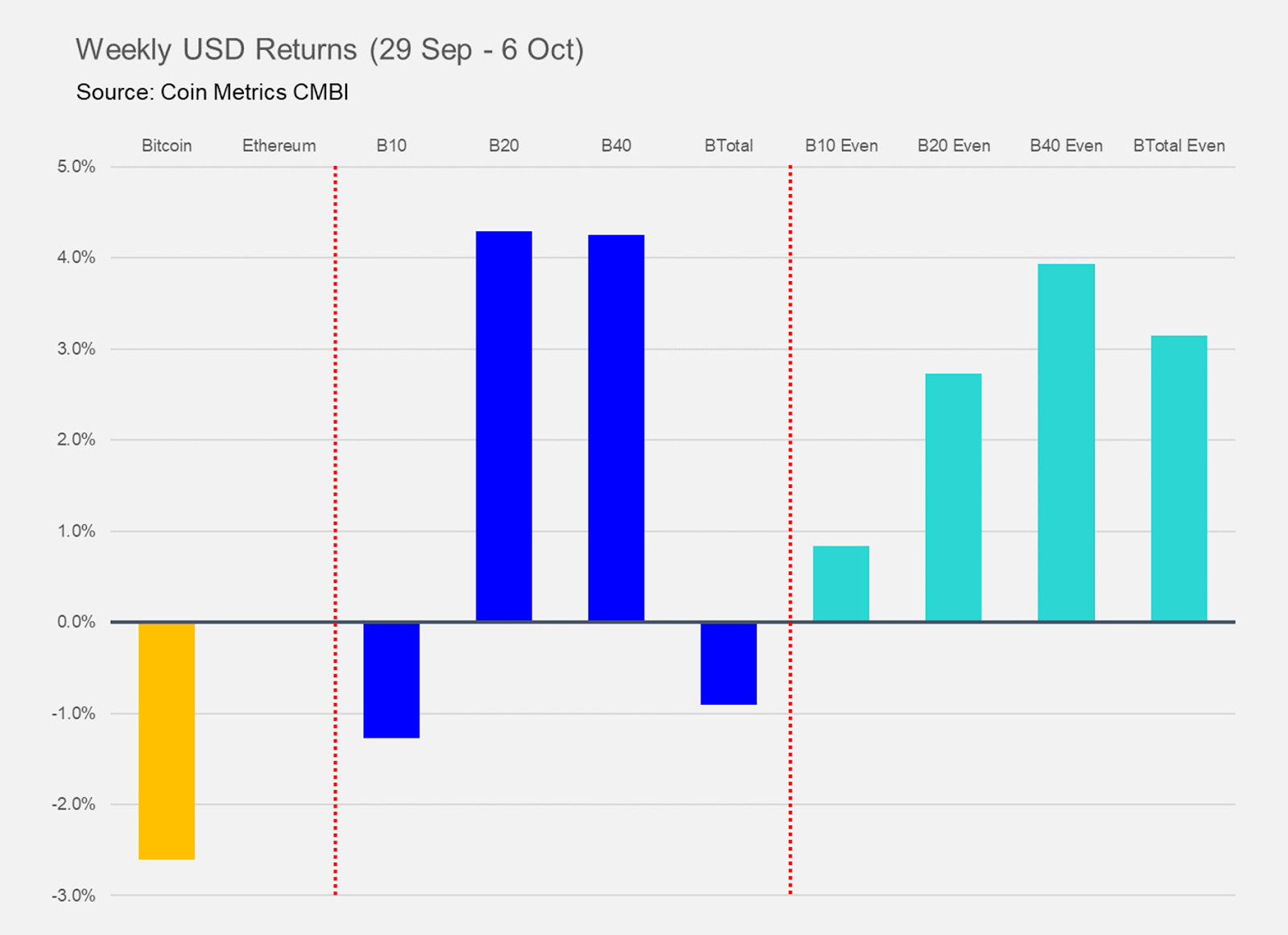

After last week's less than impressive market performance (~20% fall), mid and small cap assets rebounded the most, returning over 4% for the week as Bitcoin continued to dip (2.5%) and Ether closed flat.

At the end of the third quarter it is amazing to look at the distribution of returns across all assets over 2019. For a market that spent the majority of 2018 highly correlated on both the up side and the down side, the significant differences in return profiles (as viewed below) puts into perspective the strength displayed by large cap assets.

With Bitcoin being one of the top performers, it’s strength can further be demonstrated by looking at the returns of Bletchley Indexes in BTC terms. Interestingly, as we have reported over much of September and late August, mid cap and small cap assets have shown some recent resilience which can be seen below too.

Coin Metrics Updates

This week’s updates from the Coin Metrics team:

Coin Metrics is hiring! We recently opened up 7 new roles, including Blockchain Data Engineer and Data Quality and Operations Lead. Please check out our Careers page to view the openings.

As always, if you have any feedback or requests, don’t hesitate to reach out at info@coinmetrics.io.

Subscribe and Past Issues

Coin Metrics’ State of the Network, is an unbiased, weekly view of the crypto market informed by our own network (on-chain) and market data.

If you'd like to get State of the Network in your inbox, please subscribe here. You can see previous issues of State of the Network here.

Check out the Coin Metrics Blog for more in depth research and analysis.