Get the best data-driven crypto insights and analysis every week:

Also check out our new supplementary report: Q3 ‘21 By The Numbers

The State of the Network Q3 2021 Wrap-Up

By Nate Maddrey and Kyle Waters

In this special edition of State of the Network we take a data-driven look at crypto’s biggest storylines of Q3, 2021.

Third-Quarter Rebound

After a market wide crash to end Q2, the crypto market turned back around in Q3. BTC and ETH both finished the quarter in the green with BTC up by 32.55% and ETH returning 43.82%.

Source: Coin Metrics Reference Rates

Although BTC and ETH both had positive quarters the big winners in Q3 were newer protocols, with smart contract platforms having a particularly strong quarter. Solana (SOL), Avalanche (AVAX), and Terra (LUNA) all finished up at least 300%. Polkadot (DOT), Cosmos (ATOM), Algorand (ALGO), and Tezos (XTZ) all also had strong quarters, all up at least 90%.

Ethereum had a burst of new user adoption in Q3 largely thanks to the rapid rise of NFTs. But it also suffered from record high transaction fees throughout 2021 including a total of $1.96B worth of fees in Q3 alone. Competitive smart contract platforms like Solana and Avalanche appear to have benefited from this, as users searched for lower-fee alternatives to Ethereum. For example, SOL price surged to close to $200 in early September as ETH mean transaction fee topped $55.

Source: Coin Metrics Formula Builder

But the Ethereum community has also been hard at work addressing scalability issues. Q3 2021 saw the launch of several layer-two (L2) scalability solutions for Ethereum, including Arbitrum’s mainnet launch at the end of the quarter.

Bitcoin also saw L2 growth during Q3. The Lightning Network experienced huge growth, with the amount of BTC in open Lightning channels almost doubling from 1.67K BTC to close to 3K BTC. With continued growth in El Salvador and the recent introduction of BTC tips on Twitter, the Lightning Network is likely poised for continued growth moving forward.

Following the start of a cryptocurrency crackdown by the Chinese government in May, BTC dropped as low as $29.8K in July. After the crackdown, Chinese miners began to migrate out of the country to relocate their operations in friendlier jurisdictions. Due to the (previously) high concentration of hash power in China, the miner migration caused Bitcoin’s hash rate to temporarily drop to its lowest levels since late 2019. But hash rate started to climb back up starting on July 1st, and is now back to about the same level as the start of the year.

Source: Coin Metrics Network Data Charts

But after a rebound during the summer, the market briefly came crashing down again in September. As bullish sentiment began to take back over, ETH futures open interest climbed back towards an all-time high. On Tuesday, September 7th an unexpected price drop triggered over $2B worth of liquidations, sending the market spiraling downwards. But after the crash the market has mostly re-stabilized going into Q4, with BTC pushing back towards $50K.

Source: Coin Metrics Network Data Charts

JPEG Summer

Non-fungible tokens (NFTs) had a massive quarter and were undoubtedly one of the biggest storylines in Q3 in crypto. NFT activity far outpaced levels from earlier this year and has surprised even the most deep-seated individuals in the Ethereum ecosystem. There were a total of 9.88M transfers of ERC-721 tokens on Ethereum in Q3, a 305% increase over the 2.44M in Q2.

Source: Coin Metrics Formula Builder

The economic center of this meteoric rise was the NFT marketplace OpenSea. After registering 194K NFT purchases in Q1 and 357K purchases in Q2, there were a total of 3.8M NFT purchases on OpenSea in Q3, a staggering 965% increase quarter over quarter. The number of unique daily buyers on OpenSea averaged 17.4K in Q3, an 815% increase over the 1.9K unique daily buyers in Q2.

Signs of institutional NFT interest emerged in the markets for blue chip projects such as Art Blocks and CryptoPunks during Q3. On July 30th, a pseudonymous buyer purchased 104 of the lowest priced CryptoPunks (the “floor”) in a single Ethereum block for $7M. Then on August 23rd payments giant Visa purchased a CryptoPunk sending the average price for CryptoPunks from ~$200K to $480K (trailing 500 sales average) within a week.

Corroborating the on-chain data, Google search interest for “NFT” in Q3 also topped levels from late March/early April. However, there are some signs that the NFT market might be cooling off just a bit, perhaps as a result of heightened fees on Ethereum. The success of NFTs was a boon for ETH adoption in Q3 but likely was a key contributor to high network fees (as mentioned earlier). But with Twitter previewing NFT profile verification for its 206M daily active users, NFTs could see yet another surge in Q4.

EIP-1559

Amidst the backdrop of JPEG summer, Ethereum implemented long anticipated changes to its fee mechanism. Launched on August 5th, EIP-1559 split ETH fees into two components, a base fee which is burnt (removed from circulating supply) and a priority fee (miner tips). With over 406K ETH burnt during Q3 ($1.35B), the introduction of the burnt base fee has had a large impact on ETH’s macroeconomic policy.

Source: Coin Metrics Formula Builder

Daily net ETH issuance has come down and there have been 3 days so far with negative (deflationary) issuance.

Source: Coin Metrics Formula Builder

ETH’s issuance averaged 13.5K daily in the months just before EIP-1559 went live which translated to an annual inflation rate of about 4%. Since the launch of EIP-1559, daily issuance has averaged 6.4K implying an annual inflation rate of about 2% at today’s supply.

Looming Regulations

Going into Q4, regulators from all corners of the world are turning their attention towards crypto.

China continued its crypto crackdown to close out Q3. On Friday September 24th, China’s central bank declared all cryptocurrency activity illegal including offering trading, order matching, and token issuance services. China-based exchanges Huobi and OKEx were hit particularly hard as investors rushed to exit before the impending crackdown. On Sunday September 26th Huobi announced that it will cease all activity for users from mainland China by the end of the year. Huobi had a net outflow of $1.34B worth of ETH (440K ETH) on September 26th, by far its largest ETH outflow to date.

Not to be outdone, the United States government has also started to ramp up regulatory efforts. SEC chair Gary Gensler has compared crypto to the Wildcat banking era of the 19th century and has also narrowed in on DeFi and stablecoins. Stablecoins had a big quarter amongst the volatility of Q3, with USDC supply increasing by over 4 billion and Tether supply increasing by about 7 billion. But the supply of HUSD (Huobi’s stablecoin) dropped by about 250 million due to the regulatory uncertainty surrounding Huobi. With a Federal Reserve report on central bank digital currencies (CBDCs) reportedly coming soon, stablecoins will likely continue to come under scrutiny in Q4 as more regulators and policymakers focus on crypto.

Q3 ‘21 By The Numbers

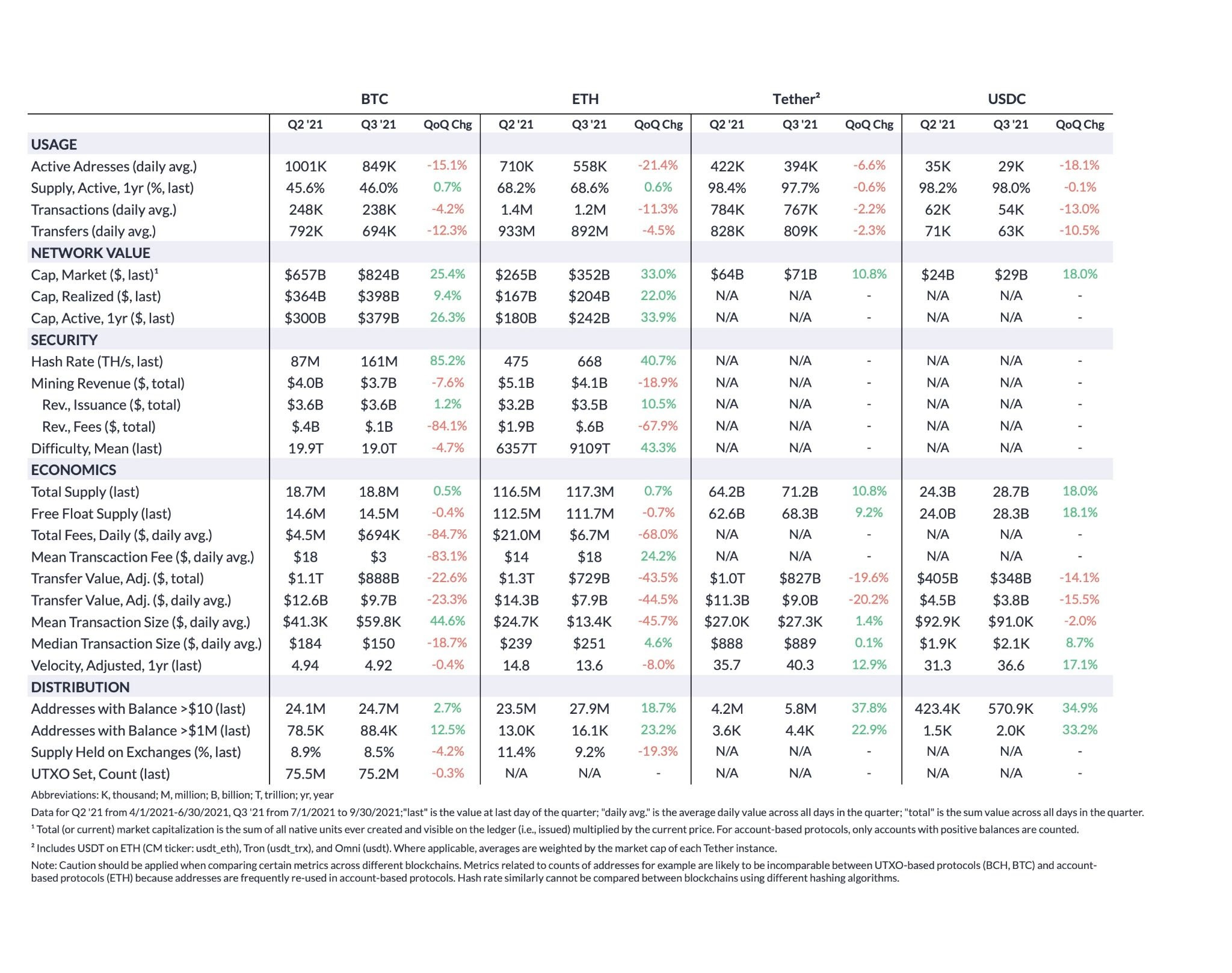

While market cap and hash rate rebounded during Q3 some of the other major on-chain metrics declined from Q2. Over the course of Q3 BTC averaged 849K daily active addresses, down about 15.15% quarter-over-quarter. ETH averaged 558K daily active addresses, down 21.4%. BTC had a total of $888B of adjusted transfer value during Q3 while ETH totaled $729B, both down from Q2.

But adoption metrics increased over the quarter. BTC closed the quarter with 24.7M addresses holding at least $10, and ETH closed Q3 with 27.9M addresses holding at least $10. Large addresses also increased, with 88.4K BTC addresses holding at least $1M compared to 16.1K ETH addresses holding at least $1M. Stablecoin adoption increased as well - at quarter close over 5.8M addresses held at least $10 worth of Tether and 570.8K addresses held at least $10 worth of USDC, up 37.8% and 34.9% respectively.

For a more in-depth look at Q3’s data trends check out our new supplementary report: Coin Metrics Q3 ‘21 By The Numbers.

Source: Coin Metrics Network Data Pro

Coin Metrics Updates

Q3 was a busy quarter for Coin Metrics. Highlights included:

We released a major expansion of our network data pro metrics, including new metrics on miner flows and EIP-1559, and also upgraded our market data feed.

In September we released a report covering the rise of NFTs on Ethereum.

We welcomed new additions to our team and are still hiring. Find our open positions here.

Coin Metrics’ Co-Founder Nic Carter and Senior Research Analyst Nate Maddrey both presented at The ₿ Word Conference on July 21st. You can view a recording of their presentations debunking common Bitcoin myths here.

Lastly, we completed a SOC 2 Type I examination conducted by Deloitte.

As always, if you have any feedback or requests please let us know here.

Subscribe and Past Issues

Coin Metrics’ State of the Network, is an unbiased, weekly view of the crypto market informed by our own network (on-chain) and market data.

Check out the Coin Metrics Blog for more in depth research and analysis.

© 2021 Coin Metrics Inc. All rights reserved. Redistribution is not permitted without consent. This newsletter does not constitute investment advice and is for informational purposes only and you should not make an investment decision on the basis of this information. The newsletter is provided “as is’ and Coin Metrics will not be liable for any loss or damage resulting from information obtained from the newsletter.